“Where Did All My Money Go?” — Surrounding Financial Goals with Simple Systems That Actually Work

The Problem

If you are earning over $250,000 per year (a great living!), you may have expected money to be a lot easier than it's unfolding to be. Not perfect or entirely stress-free, but definitely easier.

And yet, if you're completely honest, you often think things like:

- “We make too much to feel this much weight.”

- “How do we make this much and not feel like we have more to show for it?”

- “I want to get more organized and create a Plan, but life feels at capacity already.”

If that’s you, the issue usually isn’t that you’re “bad with money”.

It’s that you have good intentions—but no simple, effective systems surrounding those intentions. And good intentions without systems are just aspirations.

The Health Analogy

Most people already know the basics of getting healthier:

- Eat better

- Exercise more

- Drink less caffeine/alcohol

- Sleep more

- Stress less

But knowing you should do these things doesn't produce the desired outcomes you want (I'm preaching to myself right now too!).

Money works the same way.

You can intend to:

- Save more

- Stop overspending on things you don't really need

- Reduce your anxiety

- Give more generously

- or “finally get on a budget"...

…but if your paycheck lands in one account and life “just happens” until the next payday, the results you hope for most likely won't happen.

Why You Feel Overwhelmed by Budgeting (Even Though You’re Smart)

For high-achieving families, budgeting can feel challenging or even outright impossible for several reasons:

1) Your Life is Genuinely Full

One of the most important (and under-acknowledged) realities is this:

The season of life many high-earning families are in right now is genuinely expensive and busy.

You may be juggling:

- Demanding careers

- Young kids that demand much of your time or energy

- Coordinating childcare, activities, and camps

- High housing costs that have increased dramatically since Covid

- Travel for work or family

- Aging parents

- Church commitments

- And still trying to faithfully steward your mental, physical, and spiritual health

By the time you could sit down and "budget", your energy reserves are depleted.

2) Budgeting Feels Like a Constraint, Not Freedom

Many people associate budgeting with:

• Being told “no”

• Guilt after spending

• Rigidity that dampens freedom

And no wonder if that's the view of budgeting we have! That’s not motivating, that's debilitating.

Our brains are wired to avoid pain. And when something feels highly painful or overwhelming, most of us tend to avoid it at all costs (home projects anybody?!).

3) Spending Money is SO EASY in Today's Culture

We are constantly bombarded with ads, social-media comparison syndrome, and it takes about 5 seconds to buy something with tap-to-pay (credit cards AND cell phones!).

It’s never been easier to spend without thinking.

4) Family of Origin

Many of us never had a model of implementing financial systems or balance. A few common backstories I've seen:

- You grew up with financial scarcity, so having money now can trigger a “spend while we have the means” instinct.

- You grew up comfortable, and your parents always had nice stuff so that's your default thinking-pattern for your life.

- You never saw healthy money conversations modeled in your family.

5) You’re Operating on Autopilot

Many Americans today are frequently operating in fight-or-flight because our lives are hurried, busy, and overwhelming. And while God put our fight-or-flight mechanism in our brain for good reason, modern culture makes it challenging to cut through the noise surrounding us and get back to the unhurried life-rhythms modeled by Jesus.

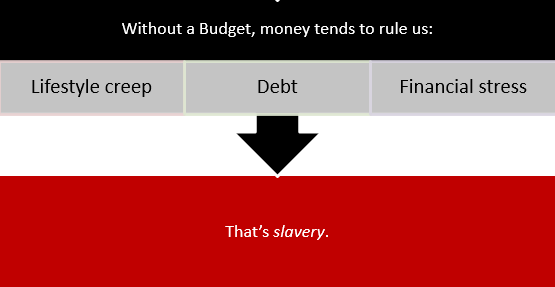

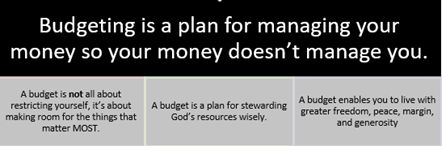

Key Insight #1: Budgeting is Freedom, Not Slavery.

I hope these 2 graphics help illustrate this point in a beautiful harmony between Truth and Grace.

Key Insight #2: Budgeting is Usually Taught Backwards

Most people operate their cash-flow like this:

- Earn income

- Spend on life

- If there's any left, then save/invest/give

This approach leaves your biggest priorities getting the leftovers. But as we all know, life is about prioritizing by what matters most. We [hopefully] do this with our time, energy, and relationships — so why shouldn't we also with our finances?

The Better Way: Work Backwards From the Life You Want

A more effective approach flips the order:

- Earn income

- Quantify how much you need to fund your biggest priorities

- Generosity goals

- Saving for a near-to-intermediate term goal or paying down disadvantageous debt

- Investing for your future needs (e.g. retirement)

- Investing for your kids' future needs (e.g. vocational-training/college)

- Then whatever remains you can confidently and freely spend —because the most important stuff is already handled

This approach allows you to tell your money where it's going before you get it. That way once you do get it, you know what's most important is being taken care of.

Rather than constantly living with low-grade anxiety and losing sleep if you're going to be okay, this system instills peace and becomes the answer to the question "20 years from now, what will you look back on and be glad you decided to do?"

The Pillars of a Good System

Now let's be totally honest for a minute. Life will happen. Things won't always fit perfectly into any system. But the goal is not to build a perfect budget. The goal is to build a system that is:

- Flexible — it's malleable to life's inevitable twists and turns [see video below for how I often incorporate this practically]

- Simple — when discretionary energy levels are low, simplicity beats complexity every time

- Time-Efficient — automate wherever possible

- Sustainable — just like switching fad-diets every 3 months likely won't get you to your health goals, burning yourself out with over-zealous financial constraints won't get you to your financial goals. It's better to stick with a good plan than quit a great plan.

The How-To System [Interactive Video]

Tangible Next Steps

- Document your biggest financial priorities (give X% of income, payoff HELOC in 12 months, save $25k for new car in 2 years, be on track for retirement at Age 60, etc.)

- Itemize each priority into a monthly dollar amount. For example, if your household gross income is $330k/year and you want to give 5% of income, that equates to $1,375 per month.

- Back into what your monthly spend budget is

- Average Net-of-Tax Monthly Paychecks (incorporate known bonuses, RSU's, etc.) minus Total Monthly Cost for biggest financial priorities determined in Step 1

- Setup your automated monthly cash-flow system (or a similar version of it) as shown in the video above

- Set a monthly reminder to review, monitor, and/or make adjustments (this shouldn't take longer than 30 minutes each month after the initial setup)

IF the monthly spend budget is simply NOT feasible for your family, I suggest working through this exercise:

- Export all your bank and credit card expenses from the Last 3 Months to a .csv [Excel or equivalent ] file.

- Sort the expenses from biggest to smallest

- Go through every transaction and simply write 1 of these 3 words in the cell next to each transaction: "Love", "Like", or "Nice-to-have"

- Once done, see if eliminating all the "Nice-to-have" items gets you to the monthly spend budget

- If it does not, you can either start removing some of the "Like" line-items, OR start considering if some of the biggest financial priorities should be adjusted (maybe retirement needs to be moved to Age 63 instead of Age 60, for example; doing this will reduce your required monthly retirement savings, giving you more cash-flow to spend month to month)

The Takeaway

If you feel like your income is high but your financial progress is low, don’t default to judgment or shame.

Most families in your stage of life don’t need more effort — they simply need a Plan and a better system.

Good intentions without systems are just aspirations.

But when you surround your intentions with simple systems that actually work, you can and will create more clarity, financial cushion, peace, and confidence that your money is allowing you to achieve what matters most in your life.

If you need help implementing this system (custom to YOU) or want a personal financial guide for the journey ahead (especially during the busy years), schedule a complimentary discovery meeting using the button below — we'd be honored to see if we could help and add significant value to your life.