The One Big Beautiful Bill Act ("OBBB Act") for $250,000+ Household Income Earners In Their 30's, 40's, & 50's

Spanning about 900 pages, the OBBB Act contains hundreds of provisions primarily related to individual taxation, student loans, 529 Plans, charitable contributions, estate planning, and health insurance.

The sheer number of changes [primarily to taxes] was honestly quite overwhelming, but I have done my best to summarize the key changes that will impact working households earning $250k+ in their 30's, 40's, and 50's in this post.

As with any big bill passed by Congress, there are several areas that will require further interpretation and/or clarification from both the U.S. Department of the Treasury and the IRS through Treasury Regulations and IRS Revenue Rulings.

Before diving into what the OBBB Act did do, let's first start with what it did not do.

Things the OBBB Act did NOT do

- Amend Social Security benefits or the taxation of Social Security Benefits

- Make sweeping changes to retirement plans (this was not a "SECURE Act 3.0")

Overall Impact of the OBBB Act

While every taxpayer's circumstances are different, the general takeaway is most taxpayers will experience a net positive impact to their taxes. The OBBB Act extended many of the more tax-advantageous laws enacted originally with the Tax Cuts and Jobs Act in 2017, with some tweaks that will negatively impact those with incomes in the $500k+ range.

Of course, everybody's situation is personal, and the effects of this massive legislation will impact everybody in different ways. So with that, I hope you [dare I say] enjoy the below!

Electric Vehicle and Residential Home Clean Energy Credits to Expire in 2025:

- Clean Vehicle Credit (up to $7,500 for new EVs) and the Used EV Credit (up to $4,000) are terminated as of September 30, 2025. Remember that there are income-limit phaseouts for these credits ($150k for married households and $75k for single tax filers [Used EV Credit] and $300k for married households and $150k for single tax filers [New EVs], although the IRS says "you can use your modified AGI from the year you take delivery of the vehicle or the year before, whichever is less. If your modified AGI is below the threshold in 1 of the 2 years, you can claim the credit".).

- The EV charging equipment credit of $1,000 (installed at your personal residence) is also eliminated for property placed in service after June 30, 2026.

- The Energy Efficient Home Improvement Credit (up to $1,200 annually for things like new windows, insulation, efficient HVAC) is terminated early – instead of running through 2032, it ends for property placed in service after December 31, 2025 .

- Similarly, the Residential Clean Energy Credit (30% credit for solar panels, etc., through 2034) is now terminated for expenditures made after December 31, 2025.

Planning Implications: If you want to hop on the train before it departs on clean energy individual tax credits (whether cars or your home) you had better act fast before they expire as early as September 30th, 2025.

Dependent Care FSA Limit Increasing from $5,000 to $7,500

Dependent Care FSA's are a tax-advantaged account offered by employers to their employees, wherein an employee can [starting in 2026] put up to $7,500 per year to pay for things for their dependent like:

- Daycare

- Nursery School / Pre-School

- Before-or-after school programs

- Summer Day-Camps (for those under Age 13)

Money put into a Dependent Care FSA not only avoids income taxes (federal & state), but is not subject to Social Security or Medicare taxes either. For a married couple earning $300,000 per year (each spouse earns $150,000), you would save $0.36 in taxes for each $1 you put into the Dependent Care FSA, meaning if you put the full $7,500 into the Dependent Care FSA, this would save you $2,704 in taxes. While the new $7,500 limit is still well below the average cost of full-time daycare, it was the first inflation-adjustment in several decades and offers parents of young children even greater opportunities for tax-savings.

NERD NOTE: While there was an increase to the Child & Dependent Care Tax Credit as well, it won't provide any additional benefit to married households with income over $210,000 per year.

Child Tax Credit Increased and Now Indexed to Inflation Going Forward

Beginning in 2025, the child tax credit will increase from $2,000 per qualifying child up to $2,200. And starting in 2026, that $2,200 will automatically increase with inflation each year going forward! The refundable portion of the child tax credit remains unchanged at $1,700 (but it was already index to inflation).

Recall that the full child tax credit is only available to households with MAGI under $200,000 (Single) and $400,000 (Married), with it completing getting wiped out once MAGI exceeds $243,000 (Single) and $443,000 (Married).

Premium Tax Credits for Health Insurance Plans Purchased via State Marketplace - Prepare to Pay More for Health Insurance & Manage Income Wisely

While not explicitly called out in the legislation, there was no extension to the "enhanced" Affordable Care Act Premium Tax Credits, meaning the enhanced health insurance premium subsidies in place since 2021 will be gone at the end of 2025 (and revert back to pre-2021 levels).

This has huge ramifications for those who plan to retire before Age 65, or those who use the marketplace for health insurance (such as the self-employed), since health insurance premiums will rise (at all income levels) or even be completely wiped out for anybody who makes more than 400% of the federal poverty line for their household size.

Below is a chart showing the % of your income you'll pay for health insurance premiums in 2026+ relative to 2025 (NOTE: the official rates ("Applicable Percentages Table") and federal poverty level for 2026 have not yet been announced as of the time of this writing, so the percentages and income-levels below will be slightly off): Note that the below is for a Household of 3 (i.e. married couple with 1 dependent child). As your household size increases, so does the Federal Poverty Level threshold.

This reduction to health insurance premium subsidies will make strategic tax-planning even more important for those who plan to retire before Age 65.

The one positive thing (mentioned below as well) is that starting in 2026, all bronze and catastrophic plans purchased on the ACA marketplace exchange will now meet the definition of a High-Deductible Health Plan, which in turn, allows individuals to contribute to a Health Savings Account ("HSA").

Health Savings Accounts

The OBBB automatically treats as a High-Deductible Health Plan ("HDHP") [which is what entitles you, among other things, to contribute to an HSA plan in the first place] all Bronze and Catastrophic level plans that are available on the individual health insurance market through the Exchange ("ACA / Obamacare plans" that are offered at the state-level), effective in 2026+. ACA plans are most often used by the self-employed and those who retire before Age 65 (when you become eligible for Medicare) — now, Bronze and catastrophic level plans that wouldn't otherwise qualify for HDHP-treatment now DO, meaning individuals can still fund HSA's up to the annual limits ($4,300 single, $8,550 married).

Also, DPC's (Direct Primary Care) are no longer a disqualifying type of coverage for having an HSA, and DPC fees can now be paid tax-free with HSA funds, as long as the fee is ≤$150/month for an individual / ≤$300/month family. DPC's are where you pay a flat fee to a primary care practitioner for unlimited visits and defined preventative care without going through traditional insurance billing each time you go in.

Permanent Extension of Lower Individual Tax Rates and Increased Standard Deduction

The lower federal tax rates we've all come to know and enjoy since 2018 have now been permanently extended (even small extra inflation bumps for the 10% and 12% tax brackets, which ironically will create a small difference between the 12% ordinary income tax bracket and the 0% long-term capital gains tax bracket). Absent the passage of the OBBB Act, the lower tax rates we've enjoyed since 2018 were set to expire at the end of 2025 and revert back to higher, pre-2018 levels.

In addition, for 2025, the standard deduction increased from $30,000 to $31,500 [Married] / $15,000 to $15,750 (Single).

And for those that remember Personal Exemptions from pre-2018, those are now permanently gone as well.

Permanent Increase to the Federal Lifetime Gift & Estate Exemption

If this one impacts you (or your parents), it's a "good problem" to have. With the new estate limit at $15 million per person, this effectively means with some basic estate planning, a married couple can pass away with up to $30 million in Net Worth and not pay a dime in estate taxes.

As a reminder, the $15 million per person limit applies to your Net Worth when you pass away, and also any gifts you've made to another person (that isn't your spouse) in excess of the annual gift exclusion limit on an annual basis (it is currently $19,000 per person per year). So if you gave away $1M to your 5 children (aggregate of $5M) during your lifetime, and then passed away with a Net Worth of $10M, you would have maximized your eligible Lifetime Gift & Estate Exemption at $15 million, and STILL not be on the hook for any federal estate taxes. Gifts from any 1 person to another (again, that isn't your spouse — that amount is unlimited) under the $19,000 limit do not count towards the Lifetime exemption amount.

However, there are still a handful of states that have their own state estate-tax threshold. Oregon has the lowest at a mere $1 million, Washington state's is $3 million, and the rest are primarily Midwest and Northeast states.

PMI / MIP Now Eligible for Tax-Deduction & $750k Limit for Tax-Deductibility of Mortgage Interest Made Permanent

For any mortgage taken out since December 15, 2017, the maximum mortgage amount you can receive a tax-deduction for is $750,000. This was scheduled to revert back to the $1 million mark, but the OBBB Act made the $750,000 limit permanent. Any mortgages taken out before December 15, 2017 are 'grandfathered' in to the $1 million limit.

New with the OBBB Act, taxpayers can now include Private Mortgage Insurance ("PMI") on conventional loans or Mortgage Insurance Premiums ("MIP") on FHA loans as tax-deductible Interest. My interpretation is that PMI interest is separate from the $750k mortgage limit, but if you have reasonably less than a $750k mortgage, you can rest assured knowing your PMI / MIP is now tax-deductible as "interest".

Remember that you can deduct interest paid on a mortgage for both primary and secondary homes, as well as home equity debt (HELOC's, HEL's) if the home equity debt was taken on to buy, build, or substantially improve the residence.

State and Local Taxes Cap Increased from $10,000 to $40,000 for Taxpayers With Less Than $500k Gross Income

Currently, taxpayers are only able to 'use' up to $10,000 per year for State & Local Taxes ("SALT") when determining if they take the standard deduction or itemize deductions on Schedule A of their tax return. Effective starting in tax year 2025, that SALT limit is increased to $40,000 for all tax-filing statuses (except Married Filing Separately, which will cap out at $20,000), but starts to phase-out if Modified Adjusted Gross Income ("MAGI") exceeds $500,000, and is completely gone (not to go lower than the old $10,000 limit) once MAGI exceeds $600,000.

The "Tax Bump Zone" For Those With Gross Incomes Between $500,000 and $600,000

The OBBB Act creates a "SALT Torpedo" or "Tax Bump Zone" where each each additional dollar of income between $500,000 and $600,000 is taxed at a higher total tax rate than the actual tax bracket they are in! Let me explain:

If you have gross income of $500,000 with itemized deductions of $75,000 (with SALT being $40,000 of the $75,000), your taxable income is $425,000.

Now if you increase your gross income to $600,000, your SALT deduction is reduced from $40,000 down to $10,000, so your allowable itemized deductions is reduced to $45,000 ($75,000 original and your SALT deduction went from $40,000 allowable to $10,000 allowable). Your taxable income is now $555,000.

The result: Your income went up $100,000, but your TAXABLE income increased by $130,000. When you do the math, that $100,000 of income actually gets taxed at a 45.5% marginal federal tax rate, even though this taxpayer is only in the 35% tax bracket ($130,000 of increased taxable income x 35%)!

Both the new $40,000 SALT limit & $500,000 of MAGI will increase by 1% each year from 2026 - 2029, then absent further legislation being passed, the old $10,000 SALT limit will return starting in Year 2030.

Alternative Minimum Tax - Preserved Higher Exemption, Lower Income Phaseout Threshold, Higher Phaseout Rate

The OBBB Act preserves the higher exemption amounts (and makes them indexed to inflation going forward) for purposes of Alternative Minimum Tax ("AMT") that have been in place since 2018 (extending how few of taxpayers will actually be subject to AMT), but it did slightly lower the income-threshold where the exemption starts phasing out (from $1.252M to $1M [Married] / from $626,350 to $500,000 [Single]), and it also increased the rate at which a taxpayer will be phased out once they have surpassed the income-threshold where the exemption starts phasing out (increasing from 25% phase-out rate up to 50% rate). This will create an "AMT Bump Zone" (where marginal federal tax rates could be ~42%) for single filers with AMT income between $500,000 and ~$675,000 and married households with AMT income between $1 million and ~$1.275 million.

Interestingly, the increase to the SALT deduction from a maximum of $10,000 per year up to $40,000 per year could push certain taxpayers with less than $600k in gross income into AMT territory faster (since SALT is NOT deductible for purposes of AMT), if that taxpayer had another AMT-Adjustment item such as exercising and holding Incentive Stock Options ("ISO's"). The greatest risk of AMT exposure falls between ~$300,000 and $500,000 of taxable income for married households, and ~$100,000 to $200,000 of taxable income for single filers.

Planning Implications: Given these new AMT amounts go into effect in 2026, it could behoove individuals with unexercised incentive stock options to potentially exercise in 2025, while the [even more advantageous] AMT rules are in effect.

PEASE Limitation Repealed and Itemized Deductions Slightly Reduced for Taxpayers in 37% Tax Bracket

In 2026+, for taxpayers in the top tax bracket of 37% (which starts at taxable income of $751,600 [Married] and $626,350 [Single]) that also Itemize Deductions, Congress is effectively reducing the value of any itemized deductions that would have provided the taxpayer a tax-deduction of $0.37 per dollar down to $0.35 per dollar.

The technical way they lay it out is you must reduce your itemized deductions by 2/37th's of the lesser of:

1) The amount of the itemized deductions;

2) the amount the taxpayer's taxable income exceeds the start of the 37% tax rate bracket.

In other words, if a married household had income of $1,000,000 and had itemized deductions of $125,000, the OBBB Act is reducing their itemized deduction by ~$6,700 (2/37th's of the $125k itemized deductions), which, at a rate of 37%, increases their taxes by ~$2,475.

Interestingly, this new reduced itemized deduction will not affect the calculation for the Qualified Business Income 20% deduction (which uses taxable income [i.e. gross income minus deductions]).

Additional Charitable Contribution Deduction For Those Who Take the Standard Deduction

Starting in 2026, the OBBB Act allows up to a $1,000 (Single) / $2,000 (Married) separate, below-the-line deduction for direct cash-to-charity donations (i.e. not contributions to Donor-Advised Funds or donations to goodwill of household goods) for taxpayers who take the standard deduction. There are no income phaseouts and no inflation adjustments on the deduction amounts.

New 'Floor' For Charitable Contributions That Are Itemized Deductions

Starting in 2026, if you itemize deductions on Schedule A of your tax return and some of your itemized deductions are charitable contributions, a portion of your charitable contributions won't count as an itemized deduction. Specifically, you will only get to include charitable contributions that exceed 0.5% of your adjusted gross income. For example, if your gross income on your tax return is $250,000 and you donated $25,000 to charity (10% of your AGI), you could only 'use' $23,750 (9.5% of your AGI) on your tax return as a charitable deduction on Schedule A. This is similar to how the deductibility of Medical and Dental Expenses has operated for years — you can only deduct medical and dental expenses to the extent they surpass 7.50% of your adjusted gross income.

Planning Implications: Due to these 2 new rules around charitable contributions, this could further enhance the benefit of bunching charitable strategies if you would take the standard deduction when ignoring your charitable contributions. For example, if you give $25,000 charitably per year, you could give $71,000 in Year 1 and itemize deductions in Year 1 (knowing you'll give out that $71,000 ratably over 3 years - $25,000 in Year 1, and $23,000 per Year in years 2 and 3), then take the standard deduction in Years 2 and 3 (while giving away $2,000 of cash directly to charity in Years 2 and 3 to benefit from the Charitable Deduction for those who take the Standard Deduction).

For a household who itemizes whether they include charitable contributions or not (i.e. they have high State & Local Taxes and/or Mortgage Interest), these 2 new charitable laws shouldn't necessitate a change to your strategy (since you itemize anyways).

Miscellaneous Itemized Deductions Permanently Eliminated, But Educator Expenses Potentially Enhanced

Prior to 2018, taxpayers could deduct "miscellaneous" itemized deductions such as investment advisory fees and unreimbursed employee expenses in excess of 2% of their Adjusted Gross Income. The OBBB Act permanently eliminates these "miscellaneous" itemized deductions, but interestingly, it seems to "shift" educator expenses (teachers, coaches, etc.) from being categorized as a "miscellaneous" itemized deductions to an itemized deduction on Schedule A (to supplement with SALT, Mortgage Interest, PMI, Medical + Dental Expenses, & Charitable Contributions). It appears it will only be able to be deducted if a taxpayer Itemizes Deductions, but if they do itemize, they could deduct educator expenses in excess of the current limit of $300 ($600 for married couples who are both educators) currently available on Schedule 1.

New Auto Loan Interest Deduction

Starting in 2025 (and through 2028), taxpayers with MAGI less than $100k (Single) and $200k (Married) can qualify for the full $10,000 per year below-the-line auto loan interest deduction (it completely phases out at MAGI of $149,000 (Single) and $249,000 (Married).

In addition to the income-limits above, the deduction only applies to:

- Loans for personal-use, new cars or motorcycles (i.e. not used) and under 14,000 pounds (i.e. excludes RV's, Trailers, ATV's)

- Vehicle must have been assembled in the U.S. —you can check the vehicle's VIN to find out

- Loan must be taken out between 2025 and 2028 (my interpretation is existing loans that are refinanced can qualify, you just can't increase the balance on the existing loan)

MAGA Accounts or "Trump Accounts"

This one is a head scratcher. So many complex, new rules that the IRS will need to issue guidance on, and not a ton of reward in my honest opinion. All I'll say is if the government makes the process to automatically get the $1,000 initial contribution the federal government is offering every US-citizen born baby between 2025 and 2027, then maybe open the account to get the $1,000. Other than that, I would fund my own money for my child's future into either a 529 Plan or UTMA.

Qualified Business Income 20% Deduction Permanently Extended and Income-Phaseouts Increased — For Business Owners and Those With Self-Employment or 1099 Income

The Qualified Business Income ("QBI") deduction allows business owners of pass-through businesses (Sole Proprietors, S-Corps, and Partnerships) to exclude 20% of their Net Profits from tax. It begins to phase out, however, once taxable income exceeds certain thresholds and whether or not your business is a Specified Service Trade or Business ("SSTB") [effectively, if your business is in the fields of law, health (doctors), accounting, performing arts, consulting, athletics, financial services, actuarial science, or any business where the principal asset is the reputation or skill of one or more of its owners or employees].

In the case of an SSTB, once your income exceeds the income thresholds, no QBI deduction for you :( If your business is NOT an SSTB, you MAY still get a deduction even if your income exceeds the income thresholds. The mechanics and nuances behind the calculation are incredibly complex and beyond the scope of this post.

The QBI deduction currently starts getting phased out once taxable income exceeds $394,600 (and phases out completely once at $494,600 - a $100k phase-out range) [Married] \ $197,300 (and phases out completely once at $247,300 - a $50,000 phase-out range) [Single]. Now, the $100,000 "phase-out range" will increase to $150,000 [Married] and the $50,000 "phase-out range" will increase to $75,000, effectively increasing the income-range where you can still obtain some of the 20% QBI deduction up to taxable income levels of $544,600 [Married] or $272,300 [Single].

There's also a small provision starting in 2026 that creates a minimum QBI deduction of $400 for taxpayers with at least $1,000 in qualified business income (meaning your deduction could be as high as 40% if you had exactly $1,000 of active qualified business income —"active" just meaning you materially participate in the business; requiring regular, continuous, and substantial involvement in the business's operations, which excludes passive investments like limited partnerships or oftentimes rental real estate).

Why QBI matters: QBI is connected at the hip to retirement plan savings (self-employment retirement plan contributions usually affect the QBI deduction you get), so it becomes paramount to coordinate the two so you are maximizing your QBI deduction while still taking advantage of tax-advantaged retirement accounts. For example, if you are married and earn $350,000/year and make a Traditional SEP IRA contribution, you are reducing your 20% QBI deduction (in other words, you're only getting a deduction for 80% of your SEP IRA contribution, but you'll have to pay ordinary income taxes on 100% of the withdrawals from that SEP IRA when you take it out!). The same can also [ironically] go for Roth contributions too!

529 Plan Expansion

Significant expansions were made to qualifying expenses for Kindergarten - 12th grade education-related expenses, including:

- Homeschooling costs

- K-12 expenses beyond tuition such as curriculum and curricular materials, books, instructional materials, online educational materials

- Tuition for tutoring by a state-licensed teacher who is unrelated to the student

- Fees for national standardized tests, AP placement exams, or college-admission exams

- College courses taken in high school (dual-enrollment fees for postsecondary programs)

The cap for these K-12 expenses was also doubled from $10,000 per year per beneficiary to $20,000 per year per beneficiary.

NERD Note: 529 Plans are sponsored at the individual state-level. This means that states can choose NOT to adopt the $20,000 per year per beneficiary for K-12 rule (Colorado's 529 is a prime example of this - Colorado also doesn't allow its 529 Plan to repay up to $10,000 of Student Loans like federal law allows). Be sure to check your state's 529 Plan to ensure it conforms to federal rules.

For Post-secondary education, 529 Plans are now able to be used tax-free for registered apprenticeship programs, recognized postsecondary credential programs, and even fees for continuing education required to maintain a recognized postsecondary credential (such as attaining the CERTIFIED FINANCIAL PLANNERTM designation as well as the ongoing costs for continuing education to maintain the certification).

A reminder here feels relevant: The primary benefit of a 529 is long-term tax-free growth (minimal secondary benefit is certain states offering a state-income tax deduction). And while I hope that these expansions by Congress to how a 529 can be used will alleviate hesitations to fund 529's from parents and grandparents, don't forget the primary purpose: Long-term tax-free growth.

Student Loans

While many provisions of the OBBB Act will be a net-benefits to taxpayers, student loans was not one of those areas. While the legislation will have the most profound impacts on future student loan borrowers (or you as the parent of a future student loan borrower), it also overhauled current federal loan repayment plans as we know them.

Let's start with current borrowers currently in repayment of federal student loans:

3 of the Income Driven Repayment ("IDR") Plans will be phased out by July 1, 2028 (potentially sooner). Those are:

- PAYE (Pay As Your Earn)

- ICR (Income Contingent Repayment)

- SAVE (Saving on a Valuable Education) - as a side, the SAVE Plan forbearance that began July 2024 will end on July 31, 2025 and borrowers will begin accruing interest on their loans under this SAVE plan.

If you are on 1 of these 3 plans, you will be transitioned out (if you don't take action) at some point between mid 2026 to 2028 and put onto either Old IBR or New IBR (existing IDR plans), depending on when you borrowed your first loan:

If your first loan borrowed was:

- After October 1, 2007 and Before July 1, 2014 - you'll be moved to Old IBR. Old IBR requires you to pay 15% of your discretionary income (excess over 150% of the Federal Poverty Line) for 25 Years of qualifying payments.

As PAYE likely won't get phased out until after July 1, 2026, if you borrowed between October 1, 2007 and July 1, 2014, you could theoretically jump onto PAYE for the next ~1 year and benefit from lower payments (as PAYE uses 10% of discretionary income and has a payment-cap)

- After July 1, 2014 - you'll be moved to New IBR. New IBR requires you to pay 10% of your discretionary income (excess over 150% of the Federal Poverty Line) for 20 Years of qualifying payments.

- Before October 1, 2007 - if you're on the SAVE Plan, your only option will be Old IBR (or RAP, once its created, discussed below), since SAVE is going away and PAYE is not eligible to borrowers who took their first loan before October 1, 2007.

Future Borrowers:

The New IDR Plan — "RAP"

The OBBB Act created a new IDR plan called the Repayment Assistance Plan ("RAP"). RAP will typically result in higher payments, because it does not determine your payment by applying a % to your discretionary income (i.e. gross income minus 150% of federal poverty line for your household size), but rather applies the % directly to your gross income. While the % starts at 1% of gross income and gradually ramps up to 10%, any household with greater than $100,000 of gross income will be subject to the 10% of gross income annual repayment formula. The only 'deduction' for RAP is a $50 per month per dependent —and while RAP does allow married filing separately status, it does not allow you to double-dip your dependents as other IDR plans have.

RAP also requires qualifying payments for 30 Years before forgiveness (the longest repayment plan of any IDR ever created), but does keep payments at 10 Years for those pursuing Public Service Loan Forgiveness ("PSLF").

However, RAP is generous in that it does not capitalize interest if your required payment is less than the interest portion of your loans. In other words, if you had $250,000 of loans at a 6% interest rate, your annual interest in Year 1 is $15,000 ($1,250 per month). But if your income is 'only' $120,000, your payment in year 1 would be $12,000 ($1,000 per month). So the RAP plan would "cover" that excess $250 per month and not add it to your existing $250,000 student loan balance over time.

RAP does conform to typical IDR forgiveness in that after 30 years of qualifying payments, your forgiven balance will become taxable income in that year (potentially generating a huge tax liability for the cancellation of debt). PSLF forgiveness under RAP appears to not be taxable (in accordance with other IDR plans) as well.

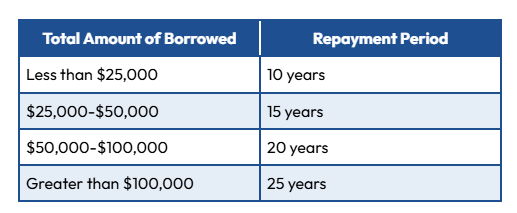

If you borrow after July 1, 2026 or consolidate existing loans after that date, RAP will be the only IDR plan available to those borrowers. The only other option aside from RAP will be a new version of the Standard Repayment Plan, and the repayment period will be determined by the amount of loans a borrower has, as follows:

New Standard Repayment Plan Repayment Period Created Under OBBB Act:

For any borrowers pursuing Public Service Loan Forgiveness (PSLF) that will have borrow more than $25,000 in loans after July 1, 2026 should note that RAP will be their only option for pursuing PSLF, given the longer repayment period imposed on the Standard Repayment Plan by the OBBB Act explained above.

New Borrowing Limits After July 1, 2026

- Graduate PLUS loans will be fully eliminated. Previously, an eligible graduate/professional student could borrow the cost of attendance minus financial aid through Grad PLUS Loans.

- Graduate loans will be capped at $100,000 for Master's Degrees, and $200,000 for Professional Degrees (law, dental, medical).

- Parent PLUS loans (where Parents can borrow for their dependent, undergraduate student(s)) are now capped at $20,000 annually, with an aggregate limit of $65,000 per child.

Parent PLUS Loans

The OBBB Act significantly changes Parent PLUS borrowers' repayment options. In order to access an IDR Plan (namely, IBR), Parent PLUS loans will need to be consolidated before July 1, 2026 and enrolled in an IDR plan (namely, ICR, as its ParentPLUS borrowers only IDR option at this point). Otherwise, Parent PLUS borrowers will only be eligible for the new standard repayment plan.

Planning Implications: With the federal government minimizing its student-loan lending liability for higher education starting in 2026, borrowers (and parents of borrowers) need to become acutely aware of the type and cost of education they plan on pursuing, with the potential to either explore more cost-effective higher education, increase savings into 529 Plans, and/or be prepared for their student to take on a much higher proportion of private student loans, which do not come with the same protections and/or flexibility that federal student loans offer.

Conclusion

The OBBB Act is easily the most sweeping piece of federal legislation impacting personal finance since the Tax Cuts and Jobs Act in 2017 — touching everything from how we calculate our taxes, to which deductions we can take, to how we save for healthcare, give charitably, and even how our kids and grandkids fund college or take on student loans.

While many of the changes will benefit high-income households in the short term — such as lower income tax rates, an expanded QBI deduction, and enhanced Dependent Care FSA limits — others require proactive planning to avoid costly surprises: like the return of the ACA health insurance subsidy cliff, new student loan repayment rules, and potentially triggering Alternative Minimum Tax.

But one thing is clear: the financial landscape for households earning $250k+ has materially changed.

If you're in your 30s, 40s, or 50s and navigating income-based student loan repayment, planning for early retirement before age 65, wanting to optimize charitable giving, or simply want a trusted guide and strategic thinking partner to help you achieve your unique financial goals — I’d love to help.

At True Riches Financial Planning, I work with households earning $250k+ for one transparent, flat fee — no product sales, no percentage-based fees — just expert, fiduciary-at-all-times advice tailored specifically to your unique path and journey ahead.