Speaking a 2nd language...Rental Property Performance Metrics

Are you frustrated your financial advisor doesn't integrate your residential investment real estate into your financial plan? Doesn't help you understand the potential returns of your rental property on a go-forward basis? Tired of playing middle-man between your CPA and financial advisor to understand the complex tax ramifications of selling your rental property? This post is for you.

At True Riches, we help clients quantify how their real estate property is geared to perform on a forward-looking basis using several unique performance metrics specific to investment real estate and run detailed analysis around the tax ramifications of holding vs selling the property (whether to diversify into a beautifully diversified investment portfolio, conduct a 1031-exchange, or even gift it to charity). And because we integrate tax-filing into our Personal CFO flat-fee service model, you don't have to play middleman between your CPA and Financial Advisor anymore either!

Why Do People Invest in Real Estate in the First Place?

The combination of passive income, leverage (i.e. debt), and preferential tax treatment can lead to phenomenal returns in residential investment real estate. Rental real estate can be an excellent way to build wealth and create financial stability. However, simply owning and renting out a rental property isn’t enough -- it’s absolutely critical to be able to understand its potential financial performance, tax benefits (or lack thereof), ratio of your returns that are liquid vs illiquid, behavioral biases of real estate, monetary liability exposure, potential time drag, and most importantly, ensuring that owning residential real estate is actually best aligned to set you up to achieve your specific life goals.

Creating Outsized Returns with Leverage - A Simple Example

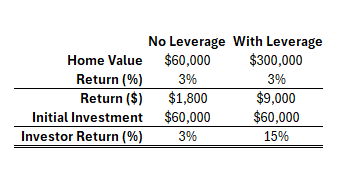

Imagine you have $60,000 you want to invest.

You could [theoretically] buy a $60,000 home for cash OR you could use $60,000 as a down payment on a $300,000 home and get a mortgage for the difference of $240,000.

In Year 1, let's say both the $60,000 property and $300,000 return 3% respectively. Now let's compare the investor return on both scenarios:

Notice the superpower of leverage - it created 5x the return compared to no leverage. It's because you as the real estate investor can participate in the full property value's returns, but only have to put a fraction of your own money in to get access to the full property value's. Of course, the flip-side of leverage is true for any negative return scenarios, and having leverage means you have a mortgage to pay too, which will effect a 2nd important measure of real estate returns -- cash-on-cash return (more on that below).

The [Potential] Tax Benefit of Real Estate - "Tax-Free" Income

You've probably seen a social-media influencer hype "tax-free passive income" with their hypothetical conglomerate Air BnB real estate portfolio (this hardly exists in reality by the way - especially with where interest rates are at as of the time of this writing). But how does it work?

First, and this is so simple, but it must be said - you have to have actual positive cash flow from your rental property to even qualify for "tax-free income". New real estate investors, especially those without a lot of funds to use towards a down payment, will not cash-flow positive for several years when first getting into residential investment real estate. Especially when you look to make your rental's "passive" by hiring a property manager who takes 7-10% off the top of your rental income and/or buying a low-maintenance property like a townhome or condo (where HOA fees eat up a lot of your rental's cash-flow).

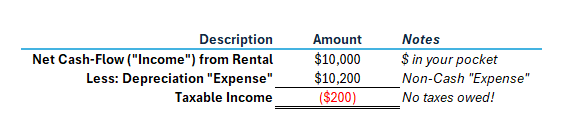

Once you have positive cash flow, the true tax-power of depreciation can kick in. Imagine you own a $300,000 townhome, and after all expenses are paid (mortgage, property taxes, insurance, maintenance & repairs, etc.) your property has net positive income of $10,000 for the year. Under normal circumstances, that $10,000 would be fully taxable to you at your marginal tax rate. But the IRS allows you to depreciate the property, and use that non-cash depreciation "expense" against the $10,000 of positive income. For the $300,000 townhome, let's assume the annual depreciation is $10,200 per year.

Now, in the IRS's eyes (i.e. through a tax lens), your taxable income looks like this:

So, even though you generated $10,000 of positive cash-flow that's now in your pocket, the depreciation 'covered' that income, sheltering you from tax in the current year. However, it must be said that unless you hold real estate until your death OR gift it to charity, depreciation serves as a tax-deferral (i.e. kicking the can on paying the tax) rather than a tax-free mechanism. If you sell the property, the IRS says "Hey! I gave you tax breaks because of depreciation all those years -- now that you're selling, you owe me that money back!" (this is referred to as Depreciation Recapture).

Behavioral Pros and Cons of Owning Rental Real Estate

Behavioral Pros:

- Forced Savings: Owning a home with a mortgage serves as a kind of "forced-savings plan" - a portion of each mortgage payment goes towards the principal balance on the loan, thus increasing your [albeit illiquid] net worth, since you are reducing your loan balance with each mortgage payment.

- Positive Habit Reinforcement: Forced savings can be equated to automation - you don't have a choice. While this can be a bad thing, some investors like the challenge of having to keep up with the mortgage payments each month - it's not really an option to just stop paying the mortgage or the property taxes - it forces perseverant, consistent behavior.

- Tangible: It is a sensory asset - you can experience it with your 5 senses - it's tangible - you can see it, feel it, etc. - and some really like that

- Stability: The natural tendency for real estate to produce less volatility than alternative investments like stocks can reduce investor's anxiety or feelings of panic during downward market movements

- Heightened Control: You are in control of the asset - who to rent to, what repairs to do or not to do, changes in rent price, etc.

Behavioral Cons:

- Illiquidity and Mental Tax Aversion Bias: If you need money from a rental property, it takes a lot of time, energy, and effort to transform it to cash. Plus, it's all or nothing (after all, you can't just sell off the guest bathroom), meaning there could be a large tax bill waiting due to depreciation recapture (discussed above) or capital gains tax from the property's appreciation since you purchased it. This strong aversion to paying taxes can lead to "letting the tax tail wag the investment dog" and ignoring the most optimal financial decision available.

- Sweaty Equity - Trading Time for Money: Absent hiring a property manager or high-HOA property (which eats into your returns), any homeowner knows the amount of time, money, and sweat it takes to maintain a home. And if you work a full-time job, have kids, want to travel, volunteer, etc. you may have to spend weeknights or weekends dealing with your investment property, leading to burnout, emotional fatigue, or anxiety over your workload.

- Overcommitment Bias & Sunk-Cost Fallacy: Investors often pour more money and time into a property to "make it work," even when returns are poor. The emotional attachment to the property can lead to falling trap to the sunk-cost fallacy.

- Loss Exposure: Many landlords do not take the legal protections necessary to shield their liability from tenants - whether that's in the form of LLC ownership (which creates administrative complexity, costs, and time) or purchasing higher levels of personal umbrella insurance for the added liability exposure (a drag on returns). This potential for personal liability and unpredictability can weigh on investors if they don't want to put money and time into protection mechanisms.

- Opportunity Cost: As with any home, the potential for unforeseen repairs and major projects requires having adequate, liquid cash-reserves available at all times in the event of a major cash need for the rented home. And those cash-reserves could be invested elsewhere generating higher returns, causing opportunity cost drag [indirectly] on the property's returns. Additionally, for new(er) real estate investors, it's likely the property will not generate positive cash-flow for several years, requiring cash-flow savings that could be going towards other investments to be used to backfill the gap in cash flow for the rental property.

How I Partner with Clients to Project Their Rental Property's Performance Potential on a Forward-Looking Basis and Quantify the Tax Impact of a Sale [VIDEO]

Concluding Remarks

Being able to measure the performance of your residential real estate investment property is essential to ensuring it is the best suited investment to meet your specific financial and life goals. It's only by being able to reasonably project key performance metrics like cash-on-cash return and return on equity ("ROE") that you can make the most informed and impactful decisions about your residential investment real estate, and how to make your money work for you and your goals as effectively as possible.

If you or someone you care about is frustrated by the lack of knowledge or ability to evaluate the potential of their residential rental properties and wants to integrate their investment real estate into their overall investment strategy while minimizing taxes along the way, schedule a free 60-minute virtual discovery meeting using the button below!