How to Give Smarter: The Mechanics and Strategic Power of Donor-Advised Funds for $250k+ Income Households

For $250k+ income households who are already using tax-advantaged accounts (like 401ks and Roth IRA's and HSA's) and still able to invest additional money into non-retirement accounts like a taxable brokerage account, there is a powerful, yet often-overlooked vehicle to save big on taxes while making a meaningful impact.

One of the most powerful tools in this space is the Donor-Advised Fund ("DAF") — a flexible, tax-smart giving vehicle that can be both a short and long term tax strategy and a unique estate and legacy planning tool.

What Is a Donor-Advised Fund (DAF)?

A donor-advised fund is like a “charitable investment account” that you control for the purpose of current and future charitable giving. It’s established through a sponsoring organization — such as DAFgiving360 (formerly Schwab Charitable), Fidelity Charitable, or faith-based sponsors like the National Christian Foundation (NCF).

Once you contribute assets to the DAF (more on that below), you receive an immediate tax deduction (because the assets are now irrevocably earmarked for charity). But here's the key: you can decide when and where to give over time, allowing you to be both strategic and prayerful about your giving.

How to Set Up a Donor-Advised Fund

Setting up a DAF is remarkably simple:

- Choose a sponsoring organization that aligns with your values.

- Open an account online — no attorney or accountant required (though professional guidance can be helpful).

- Name the account (e.g., 'The Smith Family Giving Fund') - when you give to charity from your DAF, the charity will be receiving it "from" the chosen name of your DAF account

- Fund it with eligible assets (more on that next).

- GIVE!

Many sponsors have no account minimums, and the fees are typically a fraction of the tax-savings they provide.

How to Fund a DAF

While funding a DAF can be as easy as transferring cash from your checking account into it, the real savings come from contributing investments that are not in a retirement account that have been held at least 1 year and have appreciated in value. Most often, the investments are:

- Stocks

- ETF’s

- Mutual Funds

- Digital Assets such as Bitcoin, Ethereum, XRP, etc.

- Your Privately-Owned Business

- Your Rental Property

A Tangible Example

Let’s say you hypothetically bought $10,000 of Apple stock 5 Years Ago, and it has since doubled in value — from $10,000 to $20,000.

Now suppose you’re wanting to give $20,000 to your church/charity this year. Rather than giving $20,000 from your bank account, you could give $20,000 of the Apple stock instead.

You donate the full $20,000 of Apple stock to your DAF. The $20,000 in your DAF can now be given to church/charity in the amount and timeline that you please.

Why Funding a DAF with Appreciated Investments Is So Powerful

Most Christian families give to their church or charity using cash — but this is often the least efficient way to give.

Instead, donating investments that have appreciated in value (like stocks, ETFs, or mutual funds held in a taxable brokerage account for more than one year) provides three primary forms of savings over time:

- Reduce how much of your investments will be taxable upon withdrawal (by reducing or outright eliminating the gain on the investment and through a strategy called cost-basis resetting)

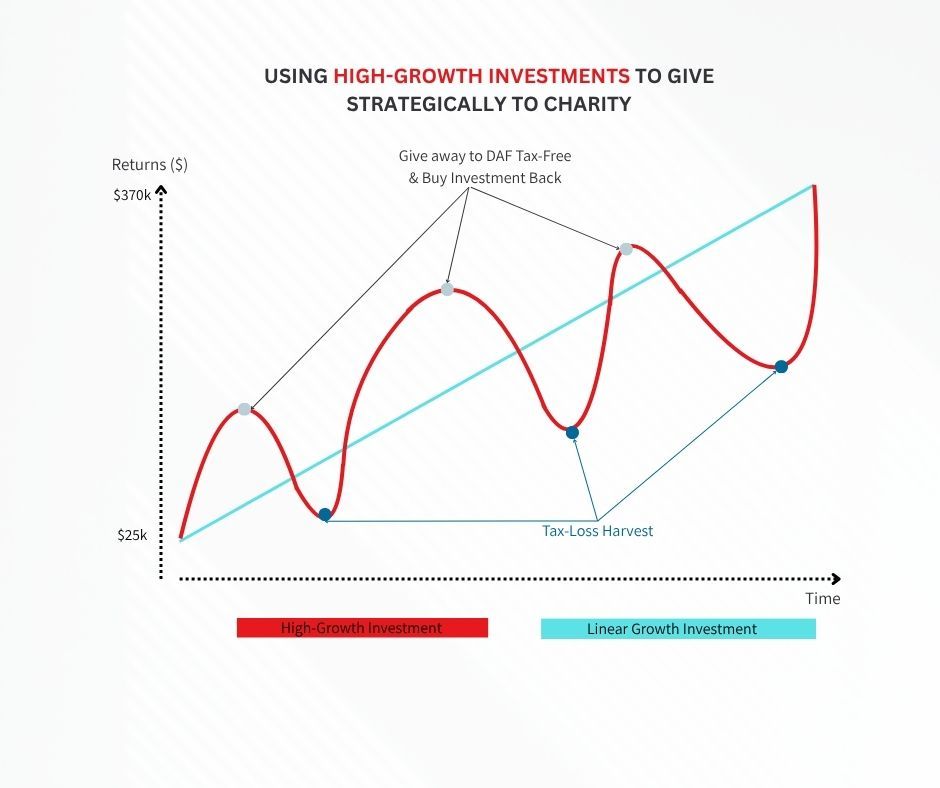

- Increased tax-savings through more opportunities to Tax-Loss Harvest your investments (see visual graphic below or watch this 90-second video)

- Increase your net worth by using your cash to buy investments that will [incredibly statistically likely] increase in value over time

Our Research

We ran in-depth case-study analysis that for a household earning $250,000 per year who saved 10% of their income and gave 10% of their income, and quantified the collective savings from the above 3 sources — which amounted to ~$168,000 in savings over a 30-year time horizon when leveraging this simple strategy compared to giving cash to charity (it did not account for more Advanced Strategies discussed below). Click the button below to view our research titled "How 1 Simple Change to Your Existing Tithe Can Save You $168,000 Over the Next 30 Years — A Strategic Giving Guide for $250k+ Income Christian Stewards"

Advanced Strategies for Using a DAF

Bunching: Maximize Deductions While Giving Consistently

With the rise of the standard deduction since the Tax Cuts & Jobs Act of 2017 (and now the One Big Beautiful Bill Act in 2025), many families come close to itemizing deductions on Schedule A of their tax return, but still take the standard deduction. But by strategically "bunching" DAF contributions, you can skyrocket past the standard deduction and accelerate a large deduction now (especially if you have a large-income event like a big bonus, large RSU vest, selling a rental property, etc.), without having to change how much you give every year. In fact, you could probably give even more because of the tax savings.

Example:

Rather than donating $25,000 each year to charity for 3 years, a couple earning $250,000 could contribute $75,000 in Year 1 to a DAF. You:

- Itemize deductions in Year 1 (and get the full $75,000 tax deduction) - for a couple earning $250,000 per year, this would equate to ~$19,800 in tax-savings in Year 1

- Use the standard deduction in Years 2 and 3, and

- Continue granting $25,000/year to your church and favorite charities from the DAF. Keep reading for how tax-free growth within a DAF could actually allow you to give even more than $25,000 per year.

Use Case

If you are approaching retirement within the next 10 years, a DAF can be an amazing opportunity to do a lot of front-loaded bunching contributions, so that you are offsetting income taxes while you're [likely] in your highest earning years (and accordingly, the highest tax bracket), and you can then give from the DAF to church/charities during your retirement.

While a DAF is a fantastic lifelong giving vehicle, it can sometimes be strategic to front-load enough to support your charitable goals until Age 70.5, then switch to Qualified Charitable Contributions ("QCD's"), which is a provision in the tax code that allows you to give money from your Traditional IRA to charity without paying tax on those dollars (and can offset your RMD once you turn RMD-age [typically Age 73-75, depending on what year you were born]).

How the Tax Deduction Works When You Donate to a DAF

When you contribute to a DAF, you receive a charitable income tax deduction for that tax year — even though you may not grant any funds to charities until months or years later.

Deduction Limits:

- Up to 30% of your AGI (Adjusted Gross Income) for appreciated investments. If your household gross income (from all sources) is $250,000, you could receive a deduction for up to $75,000 per year.

- Up to 60% of AGI for cash gifts.

- Five-year carryforward: If your contribution exceeds these limits, you can carry forward the unused portion for up to 5 future tax years.

Self-Sustainability: Tax-Free Investment Growth Inside the DAF

Once assets are inside the DAF, they can be invested in a range of tax-free investment options — including money market funds, index funds, ESG portfolios, or faith-based funds, depending on the sponsor.

Any growth within the DAF is tax-free, and more importantly, it doesn’t increase your taxable income.

Continuing the example from above where a couple earning $250,000 per year donated $75,000 to a DAF in Year 1 and was giving $25,000 per year: If we assume a modest 4% annual return, you could actually give $27,025 per year for 3 years (an 8.1% increase to your current giving) before the DAF would be depleted. If we assume 6% annual return, you could give $28,050 per year for 3 years (a 12.2% increase to your giving) before the DAF would be depleted.

DAFs as Beneficiaries of Pre-Tax Retirement Accounts

Did you know you can name your donor-advised fund as a partial or full beneficiary of your traditional IRA, 401(k), or other pre-tax accounts?

This is one of the most tax-efficient legacy giving strategies available. The results are:

- Charities pay no income tax on distributions from these accounts.

- Your heirs avoid income taxes on otherwise heavily taxed inherited IRAs.

- You reduce the [potential] taxable footprint of your estate while blessing organizations you care about (while most households no longer have to worry about federal estate taxes given the $15 million per person threshold, 12 states impose a state-estate tax at much lower levels (such as Oregon at $1 million or Washington-state at ~$2.2 million).

Structuring your estate plan this way can be a powerful way to meet your legacy charitable goals (and still support the causes and organizations you care about most) while ensuring your heirs maximize their inheritance while paying as little in taxes as possible. Best of both worlds!

Natural Rebalancing Mechanism and/or Concentrated Position Management

Tax-Efficient Portfolio Rebalancing

DAF's are also an excellent way to rebalance your investment portfolio tax-free! Rather than inefficiently selling Investment O that is overweight in your portfolio to buy Investment U is that underweight in your portfolio, you can give Investment O to your DAF and use the money you would have otherwise given to charity from your bank account to buy Investment U.

Large Concentrated Position (Company Stock, Bitcoin, etc.)

At True Riches, we often work with clients who have a large concentrated position in their company's stock through either an inheritance, equity compensation in the form of RSU's, Stock options, or ESPP shares that have been retained over the years. We frequently see company stock comprising 25%+ of a client's investment portfolio. If you find yourself asking: "How do I sell my company stock position without paying taxes?" a DAF might be a great opportunity to tax-efficiently start diversifying away from your concentrated stock position.

Just be careful as gifting RSU's, Stock Options, and ESPP all come with subtle differences in reporting the transaction for tax purposes. For example, if donating ESPP shares (and the ESPP program was a Section 423 Plan [about 80% of plans are]), you will likely need to pickup a portion of the donated shares as W2 Wage Income on your tax return for that year. If you're thinking about donating your company's stock (especially vested stock options or ESPP) be sure to work with a financial and tax planner (like True Riches) that is familiar with equity compensation taxation and strategies.

Powerful Qualitative Benefits That DAF's Provide

Simplified Tax Reporting

Since your tax deduction is claimed when you contribute to the DAF, you don’t need to collect individual receipts from each charity you later support! Your deduction is simply the fair-market value of the investments or cash that you donated to the DAF.

Ability to Incorporate Family Legacy Planning with Donor-Advised Funds

DAFs also allow you to extend your generosity beyond your lifetime. You can:

1. Name a DAF account successor (typically a spouse or children) who can "takeover" giving the remaining funds in your DAF either in accordance with your stated intentions (typically in a letter to them as part of your Estate Plan) OR in accordance with their charitable intentions and goals. We find that this allows for a wonderful opportunity to have intentional conversations about giving with your children/family, involve them in supporting the causes that are most important to you, and feel confident that you're passing on to them what matters most — a heart that is truly ready to steward wealth wisely.

2. Alternatively, you can designate "charitable beneficiaries" to receive the balance in your DAF automatically at your death. If you support 5 organizations, you could designate each of them to receive 20% of the funds remaining in your DAF, or whatever allocation you deem most appropriate.

Conclusion: The Smarter Way to Give

For high-income Christian households who desire to steward God’s provision wisely, donor advised funds offer a rare intersection of generosity, tax efficiency, simplicity, and legacy.

Whether you're in your prime earning years or approaching retirement, using a DAF strategically allows you to give more, save more, and multiply your impact over time.

Ready to Get More Intentional With Everything You've Been Entrusted? Take the first step and explore how a partnership with True Riches, the only all-inclusive financial planning practice specializing in serving Christian's in their 30's to 50's for 1 transparent flat fee, could lead you to live with more financial impact, intentionality, peace, and confidence along your life's journey.

Schedule Your Complimentary Discovery Meeting