How to Create Your Retirement Paycheck Using a Total-Return Strategy (Instead of Chasing "Income")

Approaching retirement is a big change. For decades, money has flowed into your bank account every month, and you're accustomed to adding to your accounts because you've made more money than you've spent for a long time. And if we're being totally honest, inertia is a strong force; it's really difficult to flip the direction after decades of moving one direction (not to mention the "how to" is completely different as we'll unpack!).

The question most soon-to-be-retirees ask themselves is:

“How do we turn our retirement nest egg into a paycheck that is reliable, flexible, optimized for taxes, and sustainable for the long-haul?”

For many pondering this, the default is often to what feels safest — income-producing investments like dividend stocks, bond interest, rental income, and/or income-annuities — anything that sounds like a steady income stream.

And that instinct is totally understandable. But we have to ask the question: "Is building a retirement plan around “income-only investments” actually the best way to create cash flow that is reliable, flexible, optimized for taxes, and sustainable for long-haul?

As I'll make the case for below, the answer is often no to all four of those criteria in the aggregate. And while this post is not intended to be an in-depth nor exhaustive list, these are some of the hidden problems with only chasing income-producing investments in retirement.

Potential Pitfalls of Chasing Income-Producing Investments for Your Retirement Paycheck

1. High-dividend stocks don’t reliably outperform

There’s no evidence that high-dividend stocks outperform low-dividend or even non-dividend stocks over time. Some of the most successful companies in history paid little or no dividend during their strongest growth years. And by focusing only on high-yield investments, you risk missing out on a significant portion of the market that drives long-term growth.

2. It shrinks your investable universe

If you restrict your portfolio to only dividend-paying stocks and high-yield bonds, you dramatically narrow your investible-pool and accordingly, could be missing out on the proven benefits of diversification. You might subject yourself to being overly concentrated in certain sectors (like real estate, utilities, consumer staples) and neglecting other sectors like technology or consumer discretionary.

3. Dividends aren’t guaranteed

Dividends are different than interest. Interest is contractually guaranteed, whereas dividends are simply companies you've invested in choosing to give you a portion of the business's profits. And while there are certainly companies that have paid dividends for many years, dividends can be reduced at any time [which often sends that particular stock spiraling downward]. Don't get me wrong, dividends are a slice of the pie of recreating cash flow in retirement, but they shouldn't be the sole focus.

4. Income-producing strategies can result in higher taxes

As we'll go into further depth below, income like dividends and interest is typically taxed at ordinary income tax rates, which can reduce your investment portfolio's after-tax returns through what's called "tax drag". The goal isn't to replace income, the goal is to replace needed cash-flow as tax-efficiently as possible — and there can be stark differences in taxes between these 2 approaches as we'll visually explain with a real-life example below.

5. Spending in retirement isn't a straight line

While general rules of thumb like the 4% rule is a good back-of-the-napkin approach, evidence on retirement spending research shows that spending in retirement is not a straight-line. Income-strategies often don't actually support how dynamic spending in retirement turns out to be. We'll explore this in greater detail below!

All of this may lead you to a broader realization that while income can feel 'safe', there are some costly risks that can come with this approach. Now let's talk about how a different approach, called a "Total Return Strategy", can help solve for all four needs of a retirement paycheck — reliable, flexible, optimized for taxes, and sustainable for long-haul.

The Total-Return Strategy Explained

A total-return strategy focuses on the overall growth of your portfolio from all sources (hence, "total return") rather than just the "income" it produces.

The three main sources of returns in a total-return strategy investment portfolio come from a combination of:

- Dividends from stocks or real-estate

- Interest payments from bonds

- Capital Appreciation (an investment going up in value — whether from the company's increased earnings, stock buybacks, or increased valuation of the overall company)

This 4-minute video visually illustrates each of these sources of returns. Of course, this video is not intended to be any sort of guarantee of investment performance nor investment advice.

All three of these sources of return work together to create a retirement paycheck. This approach allows your portfolio to remain diversified and growth-oriented while still supporting consistent spending.

Now lets dive into how a diversified Total Return Strategy can help create a retirement paycheck that is flexible, optimized for taxes, reliable, and sustainable for long-haul.

Flexibility of Withdrawals (Because Retirement Spending Isn't a Straight Line)

One of the biggest misconceptions about retirement is that spending will be the same every year. This makes sense not only from a common-sense point of view (life doesn't work like a spreadsheet), but also the research shows retirement spending tends to look like what we planners call the "retirement spending smile". It starts out at higher levels in the early stages of retirement (50's and 60's) during the "go-go" years [for things like bucket-list items, travel, sports, and the like] then start declining in the middle-phase of retirement (70's and early 80's) because of reduced ability or desire, then start climbing back up again in the late 80's and early 90's often because of heightened medical expenses or long-term care needs.

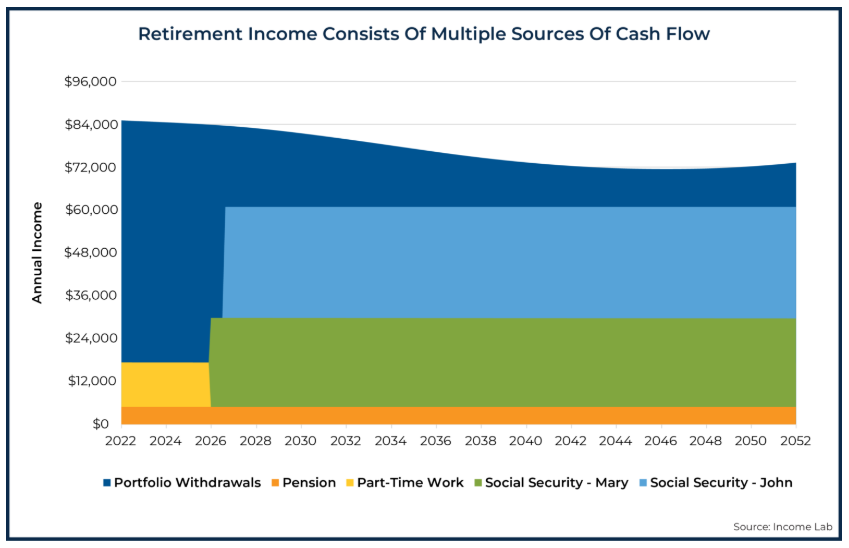

This means that static withdrawal rates (such as withdrawing 4% of your portfolio while adjusting for inflation each year) doesn't align with how actual retirement tends to work for affluent households! As we'll explore below, withdrawals from the actual investment portfolio often look like a Hatchet [depicted by the dark blue in the visual below].

Notice in the visual above, the withdrawal from the portfolio in Year 1 of retirement [before claiming Social Security] was ~$66,000, which, assuming a $1M investment portfolio, represents a 6.6% withdrawal rate. But then once Social Security kicks in and overall expenses may have even dropped in the retirees' mid-70's, the total portfolio withdrawal declines significantly (oftentimes down to a mere $12,000 per year!).

By using a total-return strategy where you build a risk-appropriate portfolio consisting of properly uncorrelated ("diversified") types of investments, you [or your financial planner managing your investment portfolio] is in the driver's seat on when to heighten distributions (to support your go-go years of early retirement) while knowing that you're not jeopardizing the long-term sustainability of your nest egg you worked your whole life to build! Contrast this with an income-only strategy that doesn’t adapt nearly as well. If your portfolio is designed to generate a fixed yield, it may not provide enough flexibility during those early retirement years when spending [and lifelong memory-generating opportunities] are highest.

Optimized for Taxes

We have to remember that before-tax returns aren't what's most important — it's after-tax returns! And using a total-return strategy is often preferential to an income-focused strategy from a tax-perspective based on how the US Tax Code is written.

When utilizing a total return strategy, you can strategically withdraw from your retirement accounts and investments to optimize for taxes (if you know what you're doing!). The Capital Appreciation element of return can oftentimes be taxed more favorably, as once you hold that investment for at least 1 year, you enter into a different (and lower) version of taxes called Capital Gain Tax Rates. On the contrary, most income-based strategies like interest, income from annuities, pensions, and some dividends are taxed at the higher Ordinary Income Tax Rates. You can also control when you "recognize income" from Capital Appreciation; you aren't taxed on it automatically each year as your investments appreciate in value.

This 2.5 minute video compares the taxes owed from an income-chasing strategy against a dynamic total-return strategy. Of course, please keep in mind this video is not tax advice nor a guarantee of paying 0% in taxes.

Balancing Current Reliability with Being Sustainable for the Long-Haul

When nearing and entering retirement, a new type of risk called "Sequence of Returns Risk" emerges. Put simply, poor investment returns in the early years of retirement (i.e. "the sequence of the returns") if not properly handled can have permanent, catastrophic effects on your nest egg. This is why tailoring the risk of your investments and ensuring appropriate diversification as you approach and enter retirement is so vital.

This is where having a tailored approach to risk comes in. While most of the attention on "risk" comes from taking too much risk (called "market risk"), taking too little risk can also be just as damaging (called "shortfall risk"). Too much in higher risk investments and you may be forced to sell at depressed values to support your retirement cash spending needs. Too little risk, and your investments may not grow enough to keep pace with inflation and keep you afloat in the later years of your retirement. This graphic helps illustrate that point by highlighting both the Pro and Con of each type of potential investment in a retirement investment portfolio, and no 1 type of investment hedges both Shortfall Risk and Market Risk [you're just taking your pick of which type of risk you want to bear].

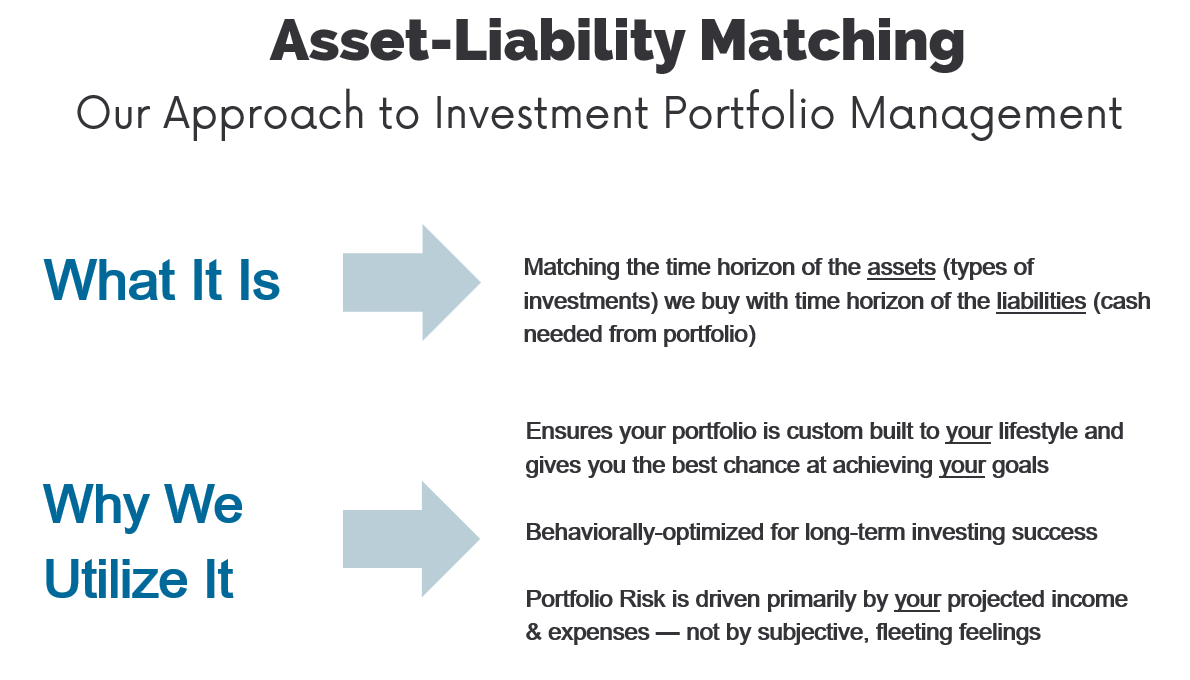

The above graphic illustrates the necessity for a thoughtful approach to creating a retirement portfolio that strategically balances Shortfall Risk, Sequence of Return Risk, Market Risk, and Inflation Risk. That's where our customized approach within a Total Return Strategy, called "Asset-Liability Matching" comes in. See 2 graphics and further commentary below.

What is Asset-Liability Matching?

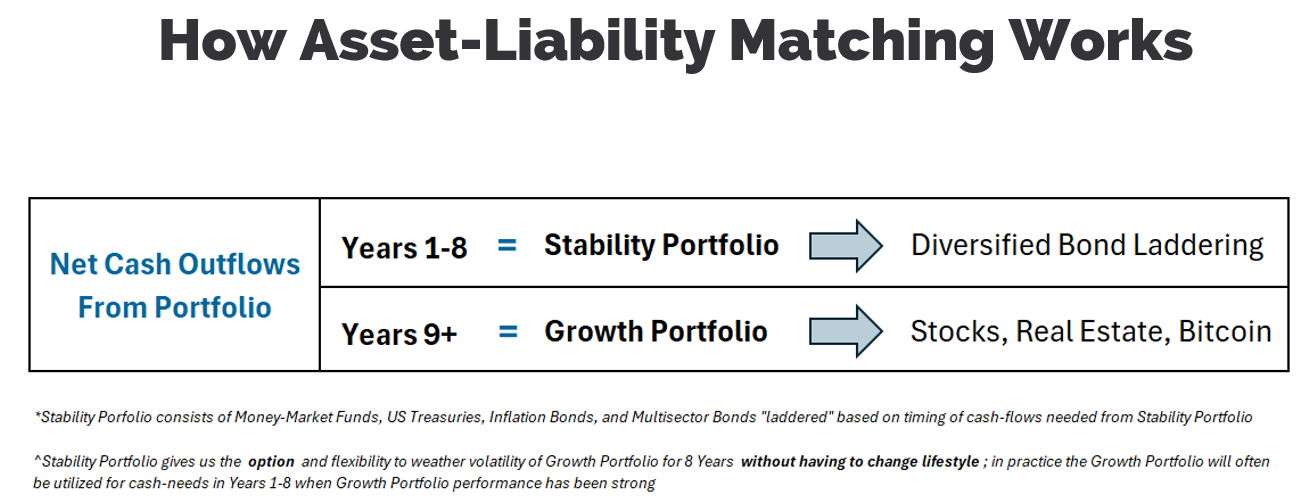

The Stability Portfolio's job is to provide for near-term retirement spending needs (Years 1-8) — money you'll need to withdraw from your nest egg for the first 8 years after accounting for inflows such as dividend income, interest income, pensions, rental income, or Social Security. As the name "Stability Portfolio" suggests, its job is to be stable, so it is invested in investments that are low-risk to provide Reliable cash-flows in retirement when the Growth Portfolio (higher risk investments like Stocks or Real Estate) are experiencing short-term volatility.

The Growth Portfolio is what will allow a portfolio to beat inflation over time and give you enough growth so you don't run out of money mid-way through retirement. But the Growth Portfolio will experience inevitable short-term swings in value ("market risk"), so we have to give it a longer time horizon (9+ Years) so the Growth Portfolio can more reliably achieve its expected long-term growth rate (historically an averaged-out annual return of about 10%).

What makes Asset-Liability Matching so powerful is it is custom-built to your retirement spending plan. Not generic 'rules of thumb' like a 50% stock / 50% bond portfolio because a risk-tolerance questionnaire told you so, but exactly aligned to recreating your desired cash flows in retirement. We do this by using financial planning software to input all guaranteed sources of income you'll have over time (Social Security, pensions, rental income, etc.) and then input your desired expenses year-over-year, and let math do the work for us!

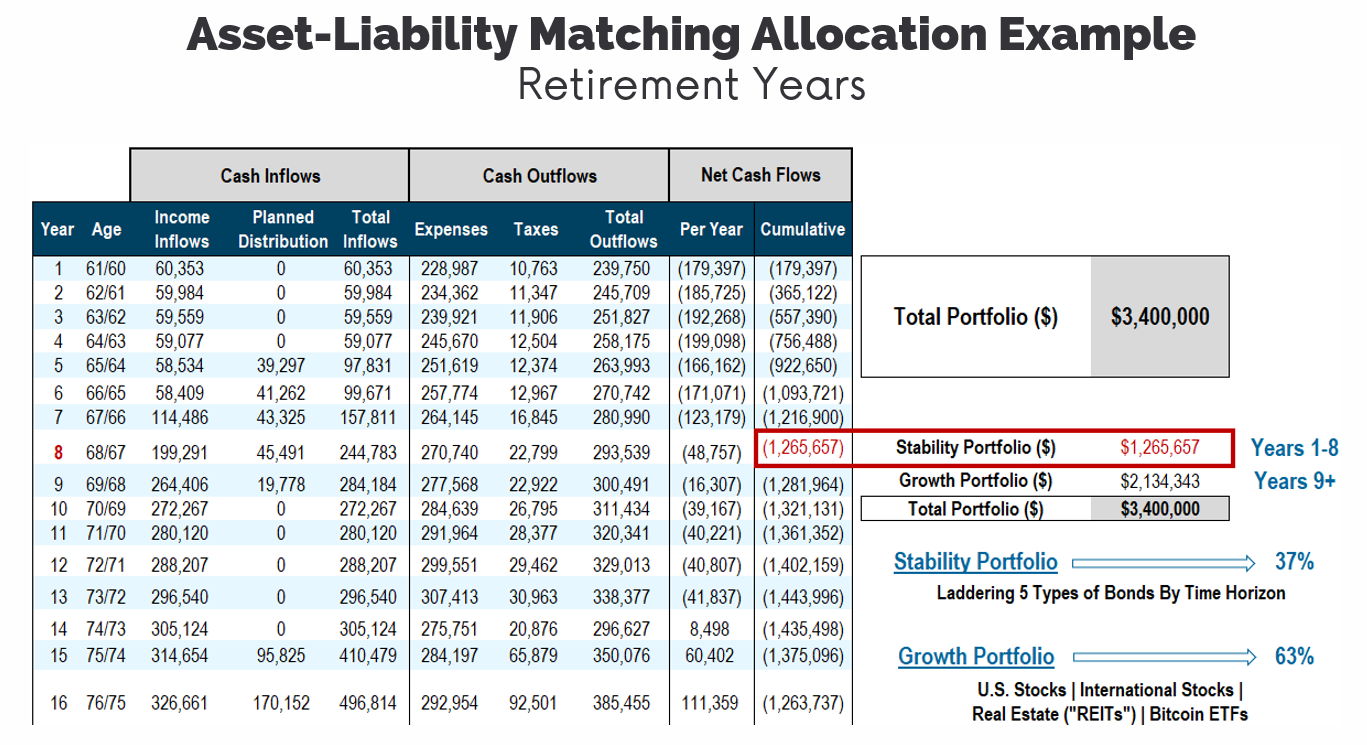

Here's an example of a retired 60 year old married couple who's guaranteed income-sources are ~$5k per month ($60,353 per year), and wants to spend about $19k per month ($228,987 per year) in retirement, and they have a $3.4M nest egg.

By letting this couple's actual desired retirement spending plan drive the risk of the portfolio (allocation between Stability assets and Growth assets), this couple feels really confident that their paycheck in retirement (~$19k per month) is reliable (because of the Stability Portfolio protecting their first 8 years of cash-needs from their nest egg) but is also going to be sustainable for the long-haul (because of the Growth Portfolio and the adequate 9+ year time-horizon it has to achieve its strong expected rate of return). Of course, this portfolio will be monitored and rebalanced over time to maintain appropriate risk through all seasons of retirement.

The Emotional Side of Spending in Retirement

Even when the math "works", spending from a portfolio can feel uncomfortable at first. Many people have spent their entire lives saving and watching their nest egg grow. Switching to withdrawals can feel like stepping into the unknown since you're relying on your investment portfolio to recreate your paycheck instead of wages from your job.

Only a thoughtful, well-designed plan helps remove that anxiety. When you understand where your cash flow ("retirement paycheck") is coming from, how long it’s projected to last, and how adjustments will be made over time, retirement begins to feel more secure.

The goal isn’t just reliability and financial sustainability. It’s having confidence and peace of mind, which is what I love about a Total Return Strategy with embedded Asset-Liability Matching.

Bringing It All Together

Creating a retirement paycheck isn’t about chasing dividends or living only off interest. It’s about coordinating all your resources — Social Security, investments, taxes, dynamic spending patterns, and your calling for retirement — into one cohesive plan.

A total-return retirement strategy allows for that coordination. It recognizes that retirement is ever-evolving over time and your withdrawal plan should evolve with it.

If you’re approaching retirement and want confidence in how your investments, taxes, and spending plan all work together to create a dynamic, sustainable paycheck, see our prospect-to-client process here and take the first step by scheduling a complimentary 1-hour Discovery Meeting.