Establishing Personal Wealth and Spending “Finish Lines”

A Practical Framework for Christian's to Unlock Radical Generosity and Live with Greater Faithfulness, Impact, and Joy

I truly believe that most devoted Christians want to live a generous life. They recognize their well-off financial position and provision, and want to be faithful stewards with their money. They regularly put money in the basket at church, or even automate a % of their paycheck to be given to their local church.

And while I am all for that and want to recognize what a good first step that is, I believe there is SO MUCH MORE God has in store for Christians who want to step into a full, abundant life and true open-handed generosity.

Today's post is [targeted] for Christians who either have household income over $250k per year OR have a $1M+ investment portfolio, and want to see how much more is possible with their generosity than simply Tithing on Net Income (even though that's a good thing).

The Problem

For most high-income ($250k+ income per year) Christians, meeting ends meet is not a problem — rather, it's a constant "tension" between the ratio of Spending, Giving, and Investing — and it continually feels ambiguous.

You might find yourself asking questions like:

- "Are we truly being Generous and faithful to our calling?"

- "How much personal wealth is enough?"

- "Can I afford to give more than 10% and still retire at a reasonable age?"

- "How do we live generously in a way that feels faithful, joyful, and sustainable rather than reactive or guilt-driven?"

The gap between biblical theology and modern financial implementation is where many well-intentioned Believers struggle. This post will introduce a practical framework for bridging the gap between the biblical invitation to partner with God to build His kingdom (through a life of radical generosity) and modern personal finance.

Why Don't Christians Give More?

Giving financially is similar to putting our faith in Christ — hardly anybody does it for purely logical reasons. Very few Christians put their faith and hope in Christ because of apologetics (even though apologetics are a good thing). The same thing goes for giving — most people don't make sacrificial changes to their financial lives based on logic alone. And there's a suite of logical reasons to give:

- The Bible is pretty clear (if you look at the comprehensive Scripture and overarching themes) about the role of money, possessions, and generosity

- Giving has been consistently studied and shown to enhance joy and overall sense of meaning/purpose

- The Golden Rule (do to other's what you hope other's would do for you if the tables were turned)

As I reflect on my own journey with generosity, here were some of the reasons my giving was limited to tithing on my net income for several years:

- Not fully informed on what the Bible says about Money, Possessions, and Generosity (lack of education and topical doctrine)

- I wanted to view myself as "generous" for the least amount of sacrifice (it's something I was obligated to do rather than had the privilege to do)

- I could give more later if I delayed giving and invested instead (a Scarcity mindset of God and neglect of the discount-rate on Impact to the recipient(s) today)

- Unaware of the statistics and crises people are facing globally (food and water shortages, malnutrition, sex-trafficking, political corruption, natural disasters, persecution of religion, etc.)

- Thinking about the hardships of others globally is disheartening (see topics above), so it's easier just to not think about it

- Desire for control and security about the future ("What if....."?)

- Desire to never be a burden on others financially if something went south with my health

- I didn't have a practical framework to inform my approach to giving, spending, and investing (accumulate as much as possible, and then if there's leftovers, I'll give more someday)

Now apply this to yourself — simply ask yourself: "Why do I give the percentage of my income that I do today? Why is it that particular amount and not a different amount?"

5 Things That Shifted My View on Generosity

1 = Education and Faithfulness to God's Word

Once I committed to prayerfully and topically studying what the Bible had to say about money, possessions, and generosity (estimated at 2,350 verses), there was no refuting the crystal clear theme in Scripture about tithing as a floor and not a ceiling (not to mention the entire heart-posture around money that God owns all "our" money anyways [Psalm 24:1, Deuteronomy 8:17-18]).

2 = Vision

The Reverse Obituary question, while somewhat logic-based, was very helpful for my generosity journey. The Reverse Obituary question sequence goes like this:

“If someone were to write my obituary based on how I handled my finances (spend, give, and invest) — what would I want it to say?" (go ahead and write it down)

Now ask yourself:

"Based on how I currently spend, give, and invest — what would my obituary ACTUALLY say about how I handle my finances?"

Lastly,

"What needs to change to bridge the gap between the two?"

The Reverse Obituary sequence isn't intended to be a guilt-trip whatsoever. They are simply a way to reflect on what matters most, and if our current living reflects what matters most. After all, it's hard to know which direction to pivot if we don't know where we currently are or where we want to go.

Once I realized what mattered most and who I truly wanted to be (I got clarity of vision), I became motivated to truly embodying the practices of a generous person day in and day out.

3 = Impact & Resounding Joy

At some point it hit me that a portion of my savings was going towards my nice-to-have wants, rather than somebody else's genuine needs. My early retirement, or somebody else being freed from sex-trafficking. My bigger house, or the Gospel of Christ being advanced and preached by brave men and women in the hardest-to-reach countries on earth.

At a certain point, excess savings puts our future wants ahead of somebody else's current needs. That really hit home for me.

And once I started giving, I found out what they say about the heart is true — it follows where your treasure goes. As I gave, it was the most fulfilling use of money I'd ever experienced, and my heart wanted to be able to give more and more and more to help those who truly need the money more than I do.

4 = The Transformative Work of the Holy Spirit

Giving generously and open-handed takes more than sound logic. It takes the heart-transforming work of the Holy Spirit as we humble ourselves under God, His Word, and His Will for our lives.

Giving is a lot like going to the gym — the hardest part is starting. I can't say I've ever left the gym and said "I regret doing that". Giving is the same way. And once you start and get a taste of the benefits, it's hard (if not impossible) to go back, because you quickly realize what a life-changing experience it is.

5 = A Practical Framework for Whole-Hearted Financial Stewardship.

Before learning about financial finish lines in 2019, giving above-and-beyond felt very ambiguous. I had no framework or plan to inform how much above and beyond I could give [while still faithfully saving for my family's future needs], or if I could actually afford to give more and not be a burden on others with the slightest misstep financially.

Through the process of financial finish lines, it also pushed me closer to God for discernment about how much I truly do need (with some margin built it). The simple question of "How Much Do I Need to Keep?" was transformative in itself, even if I didn't pursue the finish line framework at all.

What If There's So Much More Than Tithing on Net Income

My guess is — you want your obituary to say you were always open-handed and generous, excelled in the grace of giving as the Macedonian's did (despite doing so "in the midst of a very severe trial"), gave sacrificially like the Widow Mite's did in Luke 21, sold possessions for those in need in Acts 2, and beyond.

But if we're being totally honest, as we think about our current giving — it feels a lot more comfortable to autopilot towards tithing on our net income, and never thinking about it beyond that. Again, there is no judgment here, but simply posing the question:

"What if God intended so much MORE for our financial partnership with Him and advancing His purposes in the world?"

Why Establish Finish Lines?

Very few people wake up one morning and decide to pursue endless accumulation. It happens over time, oftentimes unknowingly (it's the "frog in boiling water" metaphor [a frog exposed immediately to boiling water will jump out right away, but if the water is warm initially and heats up slowly over time, the frog won't jump out and eventually boils to death]).

For most 30's and 40's Christians, incomes will increase over time. But if we don't have established, intentional "finish lines" in place, the default is endless accumulation with no end in sight. Spending and saving will increase, while generosity stays flat or even declines without the proper heart posture and habits. The world will never tell you to pursue "enough" — the only word the world knows is "MORE".

Finish lines exist to prevent that subtle drift.

The Framework: Establishing "Finish Lines" for Cash Flow (Lifestyle Spending) and Net Worth (Investment Portfolio Size).

A finish line is not a finish to work, earning, ambition, or living out God's calling. It is a finish to indefinite accumulation and building a framework that unlocks radical generosity both short-and-long term while protecting our hearts from money as our Master.

In simple terms, a finish line answers two questions:

- First, how much annual lifestyle spending is sufficient to support the life, family, and calling God has given you and your family?

- Second, how much total wealth is enough to faithfully meet future responsibilities and foreseeable needs?

Once those questions are answered thoughtfully and prayerfully, money beyond those lines can be received not as something to guard obsessively, but as surplus — margin to be enjoyed, shared, and given purposefully. The Framework visually looks like this (taken from the book "God and Money: How We Discovered True Riches at Harvard Business School by John Cortines and Gregory Baumer):

To be incredibly clear, establishing personal finish lines is not about legalism or asceticism; it's about developing discernment for true current and future needs, then applying a practical framework to add clarity, confidence, peace, and joy to that discernment.

Most clients we work with at True Riches fall into Zone 2 (make plenty of income, but haven't yet attained the level of wealth necessary to stop earning an income) or Zone 3 (have enough Wealth, but now rely on the wealth to re-create their cash-flow needs in retirement and still want to be outwardly generous towards others).

For purposes of brevity in this post, we will exclusively focus on Zone 2 using a real-life case study below, but this framework can easily be applied to all 3 other Zones as well.

Real-Life Case Study: Zone 2 (High-Income Earner Actively Building Wealth)

Background: John (Age 36) and Carrie (Age 35) are married with 2 children.

Annual Household Gross Income: $350,000

Current Investment Portfolio: $1,000,000 (retirement and non-retirement accounts, excludes home equity)

Annual Spending Needs ("Cash Flow Finish Line"): $144,000 ($12,000 per month — includes all sources of spending outside of income taxes and giving).

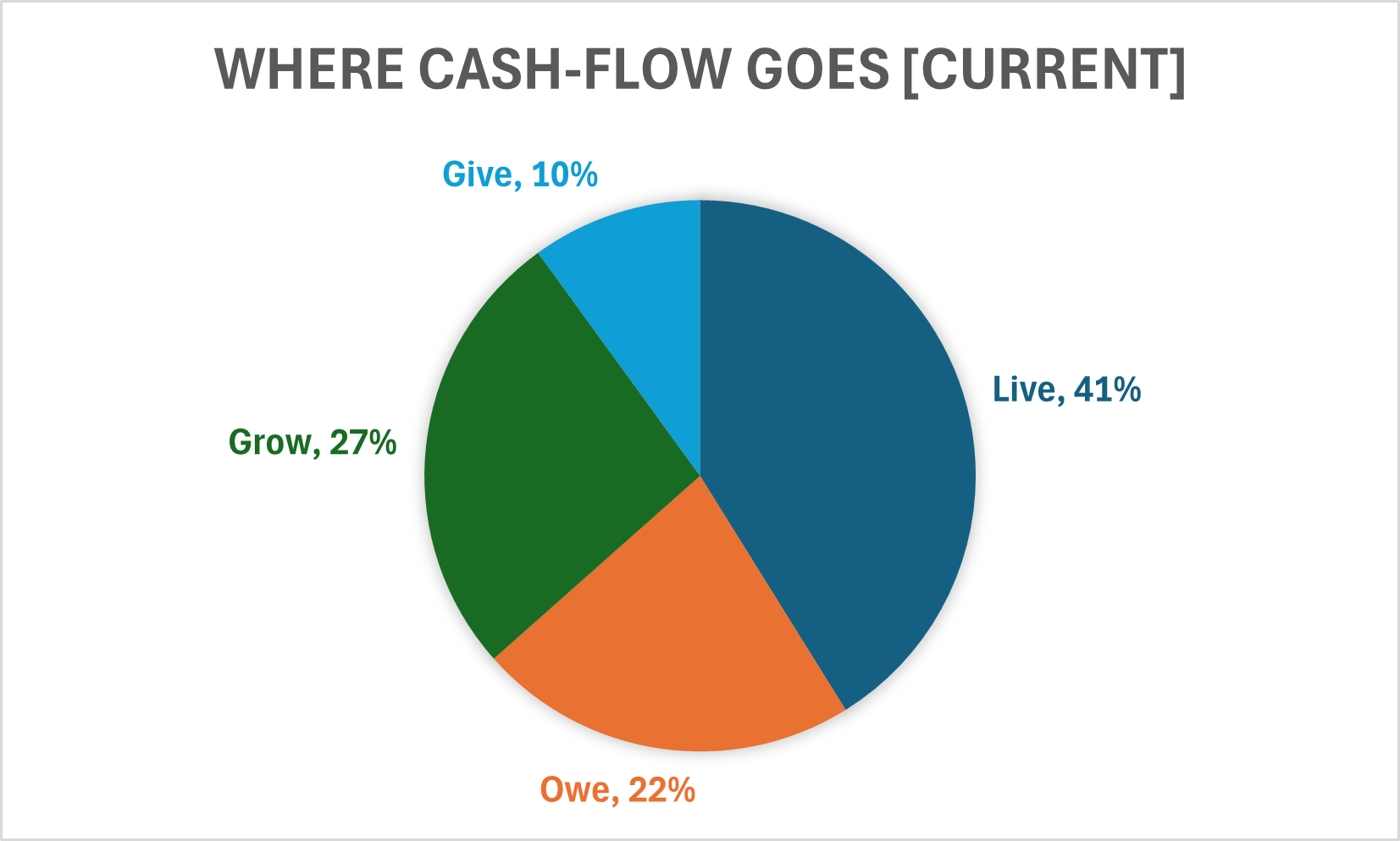

John and Carrie currently give 10% of their income, have an average tax rate of 22% , spend 41% of their income ($12k per month), and save the residual 27% of their income. Their cash-flow allocation currently looks like this:

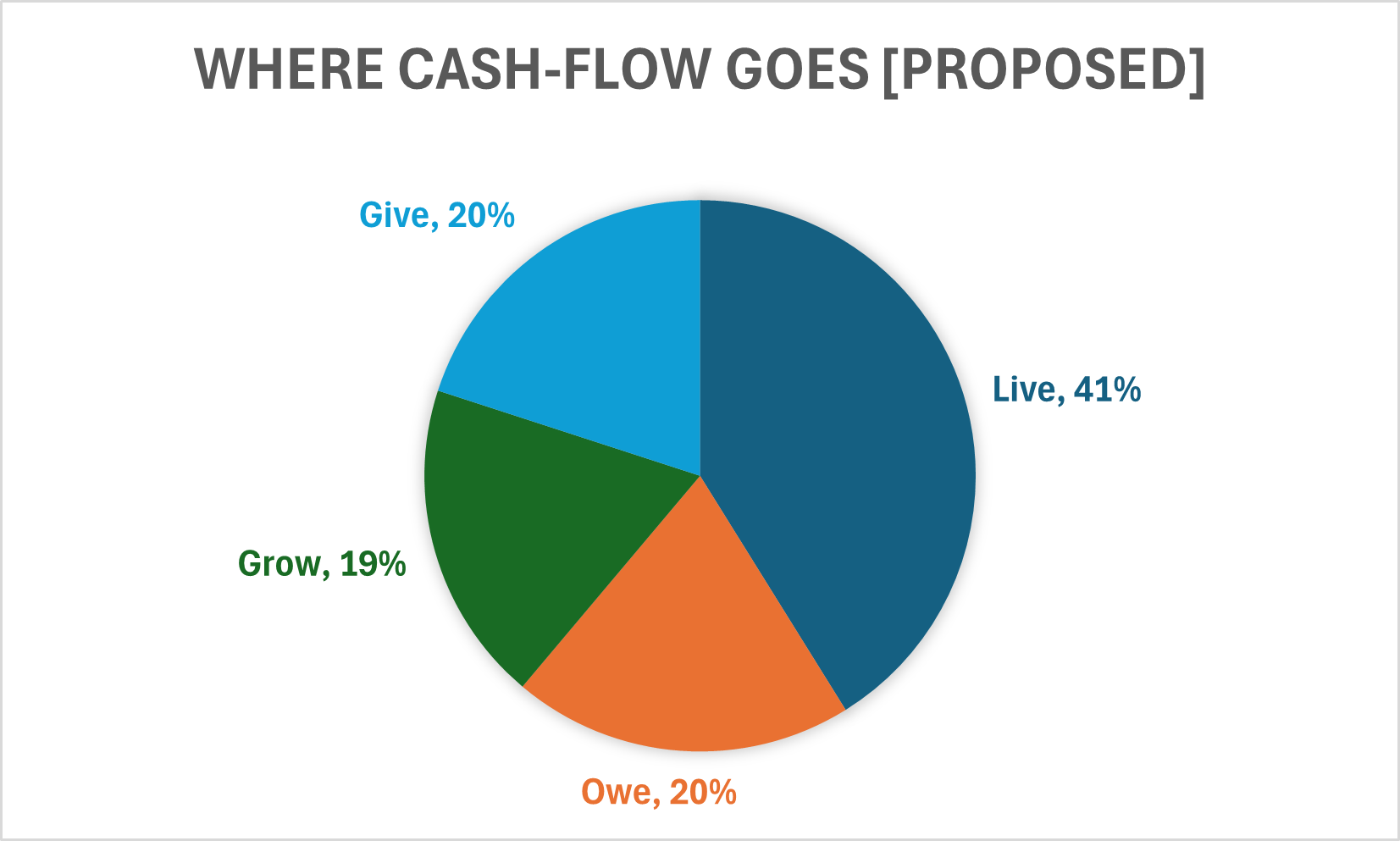

Rather than pursuing ultra-early retirement (mid 40's) or luxury vacation homes where they can "take life easy; eat, drink and be merry”’, John and Carrie love the idea of being radically generous during their lifetime. They get excited about the idea of Giving more than they Save, so they increase their Giving from 10% to 20%, and lower their savings from 27% to 19% (the increased giving of 10% lowered their tax "Owe" percentage from 22% to 20%). By planning around their cash-flow finish line of $12,000 per month (factoring in long-term inflation of course, health-care costs in retirement, and funding $30k per year [in today's dollars] for 4 years of a college-education for each of their 2 kids), they have now DOUBLED their generosity towards Kingdom-Impact, and are still on track to 'retire' (being paid for work becomes optional) by the time they are 56 years old (given their current $1M portfolio and continuing to save/invest at 19% of their income). Their New Cash-Flow Allocation would look like this:

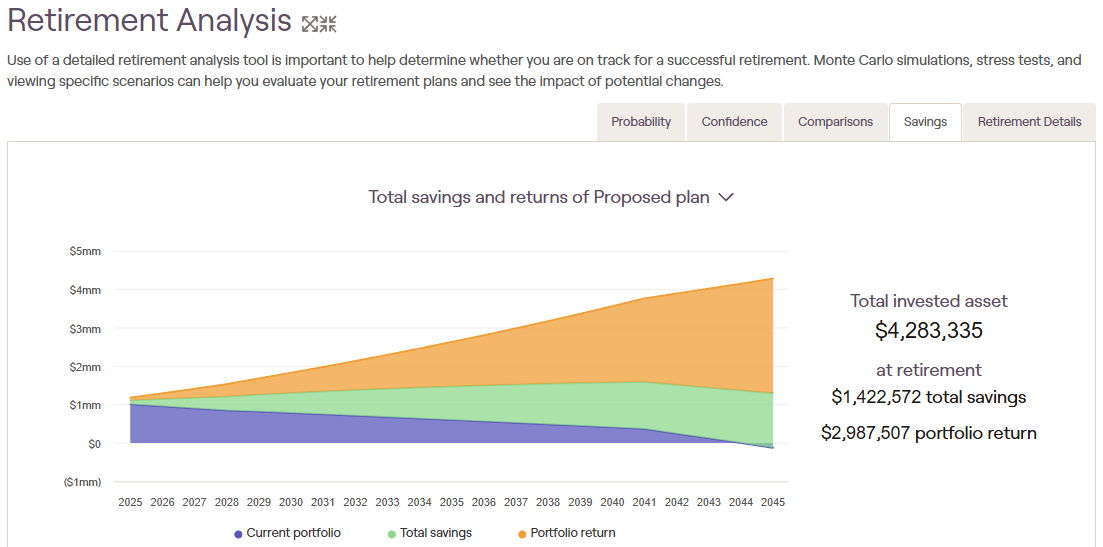

Using their cash-flow finish line and projected retirement age of 56, their wealth finish line comes out to around $4.2 million dollars to provide for their long-term financial needs. Now if income happens to increase faster than expected, market returns turn out to be more favorable than expected, or they receive an inheritance from their parents down the road, we now have an identifiable framework to inform giving, spending, and investing trade-off decisions moving forward. While of course updating their Plan will be an ongoing, iterative process, doing this intentional work up front makes for a much more impactful and fruitful life, one where generosity is fueled by joy and confidence rather than scarcity, fear, and the perpetual desire for more.

Conclusion

The Finish Line Framework is incredibly powerful and life-giving. It lives in the tension between give, spend, and invest — one that requires continual discernment with God, immediate family members, and trusted Adviser(s).

Establishing finish lines is not about perfection, but rather a framework to enable living with greater intentionality, faithfulness, joy, and life-changing Impact. And I think that's what we all crave more than anything money could ever buy.