Whole Life Insurance: Why People Buy It—and Why the Features Rarely Outweigh the Costs

Table of Contents

- Introduction

- Why Whole Life Insurance Is So Heavily Promoted

- Reason #1: Passing Assets Tax-Free to the Next Generation

- The Sales Pitch

- The Reality Check

- A Real-World Illustration: The Breakeven Problem

- The Race Analogy

- Better Alternatives

- Reason #2: Tax-Free “Income” in Retirement Through Loans

- The Sales Pitch

- The Reality Check

- Better Alternatives

- Reason #3: Tax-Free Growth on the Investments

- The Sales Pitch

- The Reality Check

- Better Alternatives

- Looking Beyond Year 8—What Happens in 20 Years?

- The Bigger Issue: Product First, Planning Second

- The Fiduciary Gap: Who Really Has Your Best Interests in Mind?

- Why True Financial Planning Beats a One-Size-Fits-All Policy

- Methodology & Assumptions (for the Case Study)

- Conclusion

- The Sales Pitch

- The Reality Check

- A Real-World Illustration: The Breakeven Problem

- The Race Analogy

- Better Alternatives

- The Sales Pitch

- The Reality Check

- Better Alternatives

- The Sales Pitch

- The Reality Check

- Better Alternatives

1) Introduction

Whole life insurance is often marketed as a financial Swiss Army knife: permanent coverage, guaranteed cash value growth, tax perks, and even a way to “bank on yourself.” And it’s true that whole life is structurally different from term life. Whole life is life insurance for well....your whole life. Not to mention many whole life policies include riders that can accelerate a portion of the death benefit for terminal or chronic illness, which can be valuable in specific circumstances.

But the crucial question is: Do these features make whole life the best way to accomplish your goals? In my experience, the three headline promises—(1) tax-free wealth transfer, (2) tax-free retirement “income” via loans, and (3) tax-free growth—are indeed true yet often inferior to what you can achieve with comprehensive financial planning.

This article uses a real illustration plus Monte Carlo simulations to show the true "cost" of whole life —and why a planning-first approach with term insurance and custom tax planning & investment strategy usually wins.

As always, this article is not intended to constitute investment advice, but general financial education.

2) Why Whole Life Insurance Is So Heavily Promoted

Follow the incentives. Whole life pays very high commissions (commonly a large percentage of the first-year premium), so there’s a built-in incentive to sell it as a universal product — and that’s how you end up with a product-first, planning-second process—reasons are retrofitted to justify the policy.

3) Reason #1: Passing Assets Tax-Free to the Next Generation

The Sales Pitch

“Life insurance death benefits are received income-tax-free by your heirs, guaranteeing a legacy regardless of market conditions.”

The Reality Check

Yes, death benefits are generally income-tax-free. But for most high-income families, there are more efficient ways to transfer wealth:

- A taxable brokerage account gets a step-up in basis at death (Translation: Heirs inherit your brokerage account investments with no embedded tax liability). With basic estate planning in place, only families with a net worth in excess of $30 million have to "worry" about strategies to mitigate potential estate taxes, which is beyond the scope of this post. But for households with less than $30 million in net worth, a simple brokerage account goes to heirs "tax-free"

- Cost drag & slow start. Whole life premiums are steep, and cash value often takes years just to catch up to what you paid in—years you could have been compounding growth elsewhere.

Note: Whole life can be a useful tool for ultra-high-net-worth households (think ~$30M+ in net worth) with illiquid estates (e.g., real estate, closely-held business) to provide estate-tax liquidity without forcing potential sale(s) of those illiquid assets upon death. Oftentimes, these whole life policies are owned by an Irrevocable Life Insurance Trust ("ILIT") so that the death benefit proceeds are paid outside of that person's estate. However, that’s a narrow, targeted use case — not a blanket reason to own whole life.

A Real-World Illustration: The Breakeven Problem

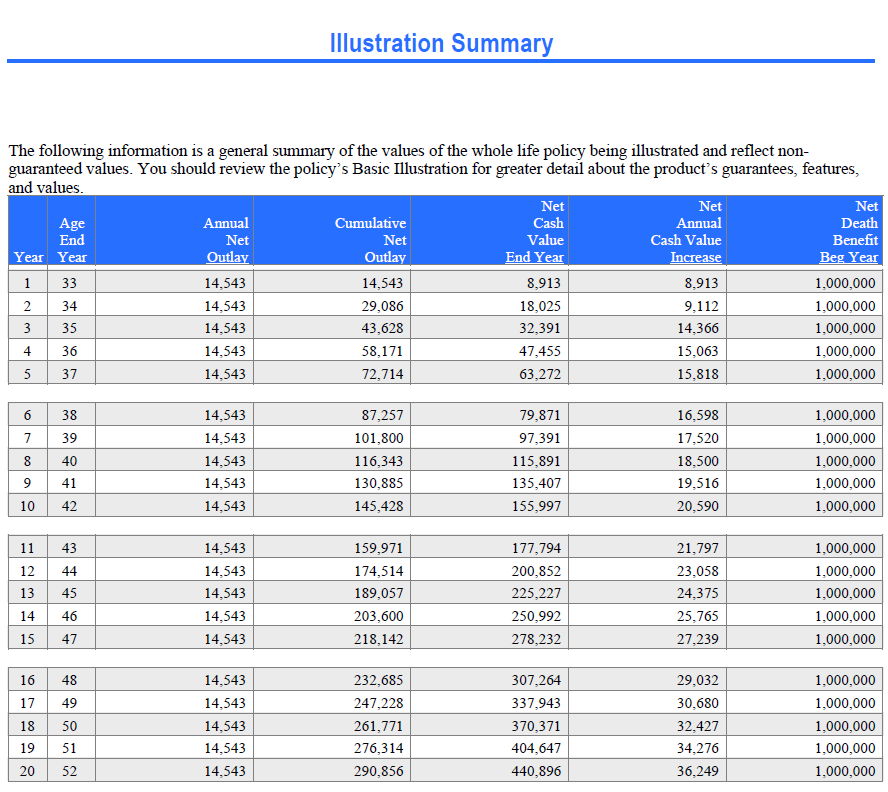

Using an actual illustration from a Whole Life 20-Pay Illustration (Male, Age 32, Ultra Preferred Nontobacco), the annual premium is $14,543 for a $1,000,000 initial death benefit with a Life Insurance Supplement Rider (LISR). By Year 8, the cumulative premiums paid are $116,343, while the net cash value is $115,891— in other words, it takes ~8 years for the cash-value to simply "catch up" to the cumulative amount put into the policy in the first place.

NOTE: While the below is a real-life illustration, there are dozens of different ways to structure a Whole Life policy, altering things such as the dividend option, pay-period, riders, etc.

Excerpted Whole Life Illustration (Years 1–8)

NOTE: “Net Cash Value End Year” reflects non-guaranteed assumptions based on the 2025 dividend scale

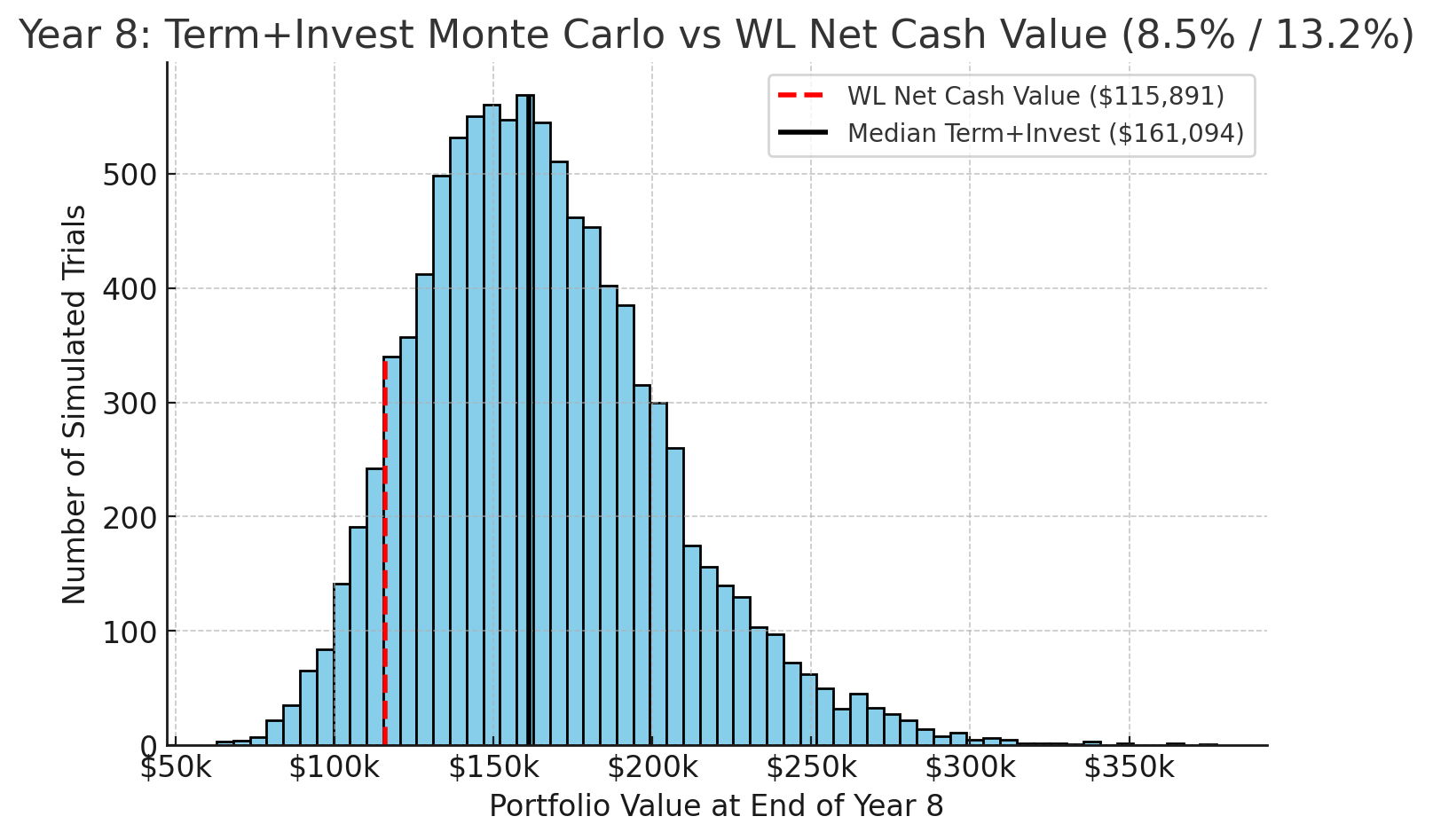

Meanwhile, a comparable $1M death benefit, 20-year Term policy costs $471/year in our case study for a 32 Year Old Male (Preferred Non-Nicotine). Over eight years that’s $3,768 in total term-insurance premiums paid — leaving ~$112,573 available for compound growth in a diversified investment portfolio.

The Race Analogy

Picture 2 runners:

- Runner 1 (Term + Invest): Buys term for $471 per year and invests the remaining ~$14,072 each year from Day 1. They start jogging towards the finish line as soon as the gun goes off.

- Runner 2 (Whole Life): Pays $14,543 into whole life annually. When the gun fires, not only do they not start running, but they roll backwards down a hill for several years. They only claw back to the starting line around Year 8. By then, Runner 1 has already made serious headway. How much headway? See Figure 1 below.

Figure 1 — Year 8 Monte Carlo Distribution (Term + Invest vs WL CV) | Term + Invest Annual Return: 8.5% | Term + Invest Standard Deviation (Risk): 13.2%

Figure 1 Key Results:

After Year 8: Whole Life Cash Value: $115,891 [red dashed vertical line] vs. Median Term + Invest Value: ~$160,657 [black vertical line]; Invest + Term Median Value = ~39% higher than Whole Life Cash Value; ~91% Probability of Term + Invest Value is greater than Whole Life Cash Value.

Better Alternatives (for Most Families)

- Term life for pure protection at a fraction of the cost.

- Invest the difference in a diversified portfolio and start compounding from day one.

- For legacy goals: basic estate planning, smart asset titling, and, if relevant, intentional charitable strategies—without locking wealth into a low-flexibility policy.

4) Reason #2: Tax-Free “Income” in Retirement Through Loans

The Sales Pitch

“Borrow tax-free from your policy—be your own bank!”

The Reality Check

- Loans against your cash value aren’t income; they’re debt. While not an exact apples-to-apples comparison, imagine I have a fully paid off home, and I decide to open a Home Equity Line of Credit ("HELOC") and borrow against the value of my home. The cash I draw from my HELOC is "tax-free", but it still incurs interest. The exact same thing is happening when you borrow against the cash value in your whole life insurance policy. The main benefit of borrowing from your whole life insurance policy is that you typically don't have to come up with the cash flow to pay the interest payments (if you have sufficient Net Cash Value in the policy to cover the loan payments), and the Net Cash Value serves as collateral on the loan for the insurance company, which is why the interest rate is favorable on borrowing against your cash value. Because if you default on the loan, or the loan starts catching up to your Net Cash Value, the insurance company has collateral that they can collect and be made whole on, which brings me to my next point:

- Policy Lapse Tax Bomb: If loans outgrow the net cash value in the whole life policy, you will either need to come up with enough cash flow to further fund the policy or the policy will lapse. In the event of a lapsed policy, the outstanding balance is taxable in that year, even if your entire cash value went towards paying off the loan! In other words, you could end up with $0 from the policy (because your entire cash value went towards paying off the loan you borrowed against), but yet you're on the hook for a potentially big tax bill!

The reality is that unless mortgage rates drop to the 3-4% range again, borrowing against whole life insurance will likely be the lowest-interest-rate form of debt available. However, keep reading to see the flip side of the coin — how much money you're truly sacrificing to have the option to borrow against your cash value at a ~5% interest rate.

Better Alternatives

- Accumulation Strategy & Coordinated Withdrawals: Optimize tax-location of investment accounts across taxable accounts (brokerage), tax-deferred accounts (401k/403b/IRA), & tax-free accounts (Roth IRA, HSA) to minimize lifetime taxes upon withdrawal. Utilize Roth conversions, tax-loss harvesting, capital gain harvesting, QCD's, DAF contributions, etc. to minimize tax burden over time.

- Cash Flow Flexibility: Adjust savings and needed withdrawals to life changes. Whole life premiums are typically rigid and high in the early years. If your income drops or life circumstances change, you can’t just “dial payments down” in the early years of a policy (because there's hardly any Net Cash Value yet) like you could with a brokerage account or 401(k) or Roth IRA or HSA.

5) Reason #3: Tax-Free Growth on the Investments

The Sales Pitch

“Cash value grows tax-free… like a Roth IRA!”

The Reality Check

Cash value compounds tax-free inside of the whole life insurance policy. And a policyholder can withdraw up to their Cost Basis (what they've put into the policy) tax-free at anytime (just like a Roth IRA). The difference, however, is that unlike a Roth IRA, you can't actually withdraw the earnings/growth of your whole life policy tax-free like a Roth IRA [After Age 59.5] — with whole life, you have to borrow against it, which as we discussed earlier, incurs interest costs because borrowing is debt, not income. So yes, the cash-value grows tax-free, but it is not cost-free when needing to access cash from your policy.

Whole life insurance [typically] grows as a result of a modest interest rate plus non-guaranteed dividends from the insurance company. And while it's good that the cash value will grow over time, the long-term returns of whole life will [statistically likely] drastically lag those of investing in a diversified portfolio consisting of stocks, bonds, real estate, etc. This makes sense because underlying cash-values have to be invested entirely in bonds (primarily high-grade corporate bonds and government backed bonds), so the risk and return potential are understandably lower. And while many sales pitches will appeal to this risk-aversion of investors ("you'll avoid the market crashes") it is simply introducing a different form of risk called Shortfall Risk.

Shortfall Risk is the risk your investments will not grow enough to combat the long-term effects of inflation — your "real returns" (returns net of inflation), won't be sufficient to have your portfolio sustain itself for the long haul. And Shortfall Risk is oftentimes just as big of a risk to young investors (30's to 50's) as it Market Risk (the underlying volatility of risk-bearing investments like stocks or real estate). The sales pitches for whole life insurance are preying on what is called Loss Aversion Bias, which is the human psychological tendency to avoid pain — in other words, most humans agree that the pain of losing 100 'units' hurts more than the pleasure from gaining 100 'units'.

I'm the first to acknowledge there are no guarantees in life; change is inevitable, and we aren't even guaranteed tomorrow. But no matter what you do with your money, whether it sits entirely in cash under a mattress or you own 100% meme coins, both are taking risks. The mattress cash-hoarder is taking on Shortfall Risk, and the 100% meme coin owner is taking on tremendous Market Risk. I believe the key is taking calculated risks when it comes to long-term financial planning decisions, which is part of why at True Riches we employ a low-cost, tax-efficient, broadly diversified investment strategy that is tailored to each individual household we work with.

Better Alternatives

- Utilize tax-advantaged accounts first (401(k)/403(b), 457(b), HSA, FSA, Roth IRA, 529), aligning the risk of the underlying investments with the time horizon for each tax-advantaged account

- In taxable brokerage accounts, use tax-efficient investments, maximize tax-loss harvesting opportunities, and use appreciated investments to strategically give to charities or your church

- Let your entire financial life plan dictate asset location, rebalancing, and eventual withdrawal strategy

6) Looking Beyond Year 8—What Happens in 20 Years?

A common sentiment: “Whole life is slow early, but catches up if you give it time.”

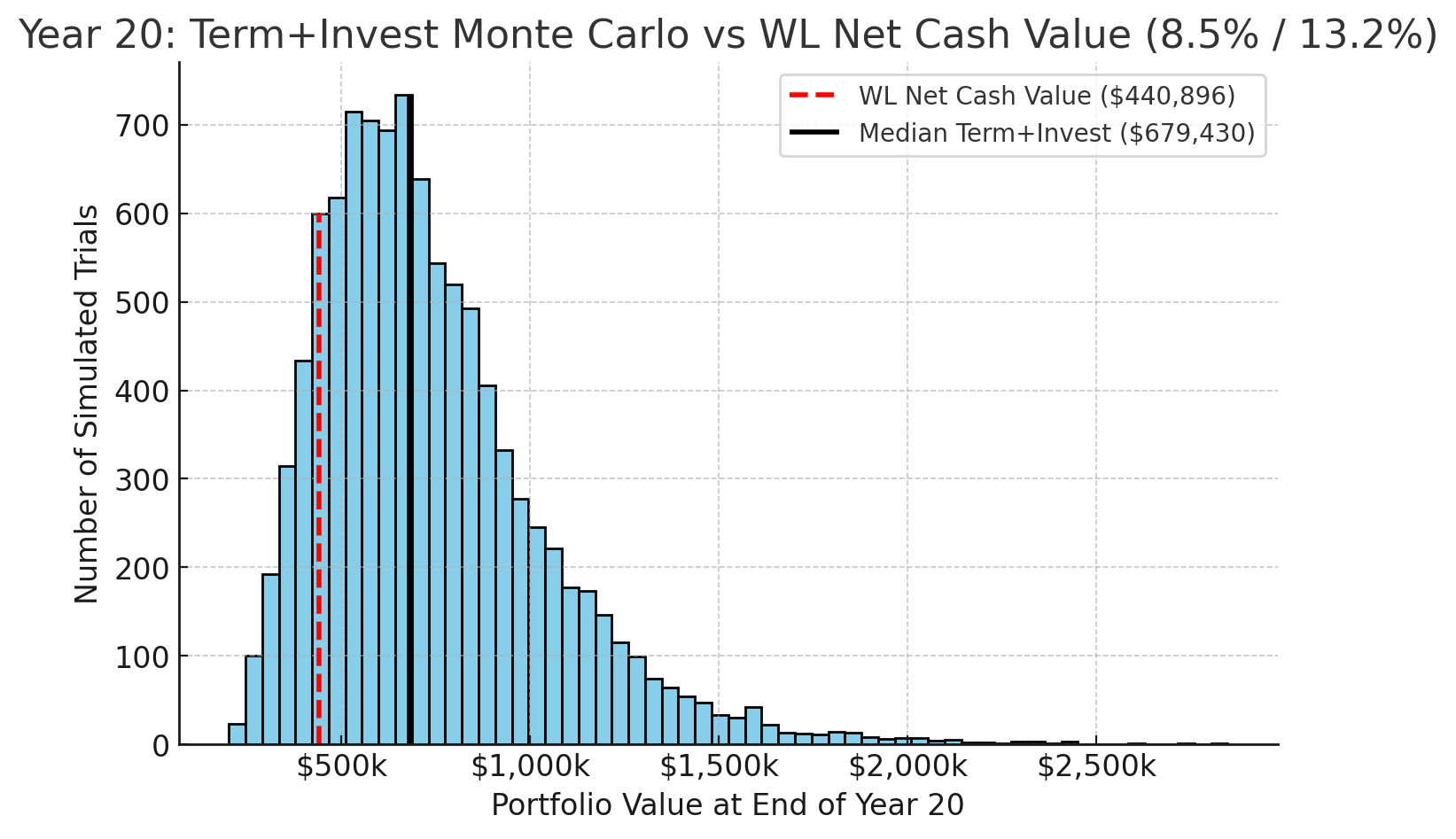

Let’s test that claim with the same case study, but extrapolated out to 20 years. See Figure 2.

Figure 2 — Year 20 Monte Carlo Distribution (Term + Invest vs WL CV) | Term + Invest Annual Return: 8.50% | Term + Invest Standard Deviation (Risk): 13.2%

Whole Life Net Cash Value, Year 20: $440,896

Median Term + Invest, Year 20 Median Value: ~$686,404

Term + Invest advantage: ~56% higher ending value than whole life at the median

Probability that Term + Invest beats whole life (Year 20): ~88%

Interpretation: Even with 20 years of runway, the gap doesn’t close—it widens. Compounding is working against policyholders who sacrificed early-year growth.

Now I ask the [hopefully rhetorical] question: Is being able to borrow against $440,896 at a 5% interest rate better than strategically drawing down $686,404 and paying 10%-20% in taxes? To reiterate, whole life insurance does have some features that make it attractive, but when you consider all the factors, the pros of the 'features' don't make up for the downsides of whole life insurance in the first place.

7) The Bigger Issue: Product First, Planning Second

Whole life is frequently sold as the centerpiece of a plan. That’s backward. Planning should drive process, which then dictates strategies.

With a plan, you scale retirement savings up or down, revise tax strategy in alignment with your annual cash flow and lifestyle goals, and recalibrate insurance needs as life inevitably evolves.

8) The Fiduciary Gap: Who Really Has Your Best Interests in Mind?

Insurance agents are not fiduciaries. They’re typically paid via commissions, and are not obliged to recommend the best (or lowest-cost) solution. Fee-only fiduciary planners, by contrast, are paid transparently and are obligated to put your interests first. That alignment tends to reduce product bias and increase planning quality and transparency.

9) Why True Financial Planning Beats a One-Size-Fits-All Policy

- Tax strategy integration: Strategic Roth conversions, capital-gain harvesting, asset location, tax-loss harvesting, QCDs, DAF “bunching,” etc.

- Customized estate planning: Appropriate titling, intentional beneficiary designations, use trusts when absolutely needed

- Behaviorally-sound investing: A diversified, low-cost, tax-efficient portfolio aligned first and foremost with your lifestyle goals — if you don't know what you're investing for, it's going to be difficult to know how to properly invest

- Cash Flow Flexibility: Adjust contributions, spending, tax-strategy, and withdrawals as your life changes.

When whole life can make sense: UHNW families (≈$30M+ estates) with illiquid assets may use permanent insurance for estate-tax liquidity. For most others, it’s an expensive solve to a problem that better holistic planning already addresses.

10) Methodology & Assumptions (for the Case Study)

Illustration: Whole Life 20 Pay (Male, 32, Ultra Preferred Nontobacco). Annual premium: $14,543; Initial death benefit: $1,000,000; LISR included; loan rate shown 5.67% adjustable; dividends not guaranteed. The Year-8 summary shows cumulative net outlay $116,343 and net cash value $115,891 (non-guaranteed basis), i.e., roughly breakeven at Year 8. Year-20 net cash value: $440,896.

Term premium: $471/year, 20-year term for comparison (Male, 32, Preferred Non Nicotine).

Investing the difference: ~$14,072 contributed at the start of each year.

Simulation: 10,000 Monte Carlo paths using 8.5% geometric mean return and 13.2% standard deviation (risk); independent annual draws; no advisory fees, taxes, or trading costs applied

Key results:

Year 8: WL CV $115,891 vs. median Term + Invest ~$160,657 (≈39% higher); ~91% probability Term + Invest > WL.

Year 20: WL CV $440,896 vs. median Term + Invest ~$686,404 (≈56% higher); ~88% probability Term + Invest > WL.

Important caveats: Simulations are educational, not predictive. Actual WL dividends, loan terms, policy changes, taxes, fees, and market returns will vary. The Whole Life document itself emphasizes that non-guaranteed elements (dividends, LISR term costs) can change and that policy access/loans reduce values and can trigger taxes on lapse.

11) Conclusion

Whole life is often sold on three overinflated premises —tax-free death benefit, tax-free loans, & tax-free growth—but the features generally don't make up for the shortcomings:

- The breakeven drag is real: our case needed ~8 years just to catch up to cumulative contributions put into the policy.

- Term + Invest outperformed ~91% of the time by Year 8 and was ~56% higher at the Year-20 median, still beating Whole life ~88% of the time.

- Whole life’s inflexible, high premiums create cash-flow risk, which is dangerous in the early years when cash value is low and lapse risk is higher if life circumstances change.

- For most families (especially under the current high estate-tax exemption), basic estate planning and a diversified portfolio will transfer wealth and build flexibility more effectively.

- Exception: UHNW, illiquid estates may use permanent insurance for estate-tax liquidity—a targeted solution, not a default one.

Bottom line: Don’t let a product define your financial life. Let comprehensive planning lead the process and strategies.

🎯 Ready to Explore What’s Possible?

True Riches is an independent, fiduciary-at-all-times, flat-fee-financial planning practice that specializes in helping $300k+ income Christian households simplify their finances, develop a comprehensive plan, and provide advice that's always in their best interest so they can maximize their life’s impact and experience greater calling, peace, and confidence along the way.

We offer a complimentary 60-minute Discovery Call to help $300k+ income Christian households best align their resources and strategies with what matters most to them.